Three months after he launched his war on Iran and more than a week after he said an extension of the ceasefire that he declared on April 7 was “largely negotiated”, President Trump says he’s finally ready to make a decision on whether to accept the terms that have been agreed between the countries’ negotiators. But he hasn’t yet. Iran’s Supreme Leader Mojtaba Khomenei has also so far refused to approve it.

The deal on the table appears to be the same as it was last week: an extension of the rather shaky April 7 ceasefire for another sixty days with an end to the US blockade and Iranian attacks on shipping, which would allow oil to once again flow through the Strait of Hormuz. The agreement leaves the difficult questions of Iran’s nuclear fuel, frozen assets, reparations, sanctions, and stewardship of the Strait for future discussion. On all of these issues, it appears, the two sides are still far apart. Trump has accepted that Iranian assets could be unfrozen but only if Iran commits to never having nuclear weapons (it has said for years that it has no intention of having them) and hands over all of its nuclear fuel (something it refuses to do). The US — indeed, all countries — rejects the idea of Iran charging a toll or restricting in any way passage through the Strait.

Despite these differences, as I had expected market participants have over the past ten days traded as if the war is coming to an end. Spot oil prices have fallen about 20%, government bonds and equities have rallied and save-haven flows into the US dollar have partially reversed.

These differences could mean that we find ourselves in two months pricing in new restrictions on oil flows and renewed fighting. My bias, though, is that both sides are sufficiently motivated to reach a ‘permanent’ end to the war that some kind of deal will be agreed to allow both to declare victory and for Trump to bring most of the US troops home. Despite what he said last week, I think Trump does want to see oil and gas prices come down fast enough that they aren’t a liability during the mid-term election campaign.

But the Middle East will not return to the status quo ante. First, the ceasefire extension under consideration doesn’t appear to apply to Israel, and probably therefore will not be seen by Iran as preventing their proxies in the region from continuing to attack US allies or shipping. It’s not even clear that Trump would agree to bind Israel in any final deal with Iran. Second, we now know that Saudi Arabia and the UAE not only facilitated US attacks on Iran but launched attacks of their own against Iran. Even if Trump ends the US’ involvement in the conflict, risks to shipping in the Strait will remain high until all countries in the Middle East agree to terms.

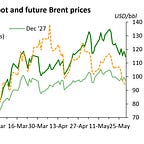

Therefore, while spot Brent prices have fallen about 20% from their highs of about ten days ago, December 2027 futures have fallen only 4%. Those futures prices have traded within a USD75 - 80/bbl range for the past six weeks. Even in an ideal situation, it will take many months for oil markets to re-equilibrate — and even longer for natural gas and refined products.

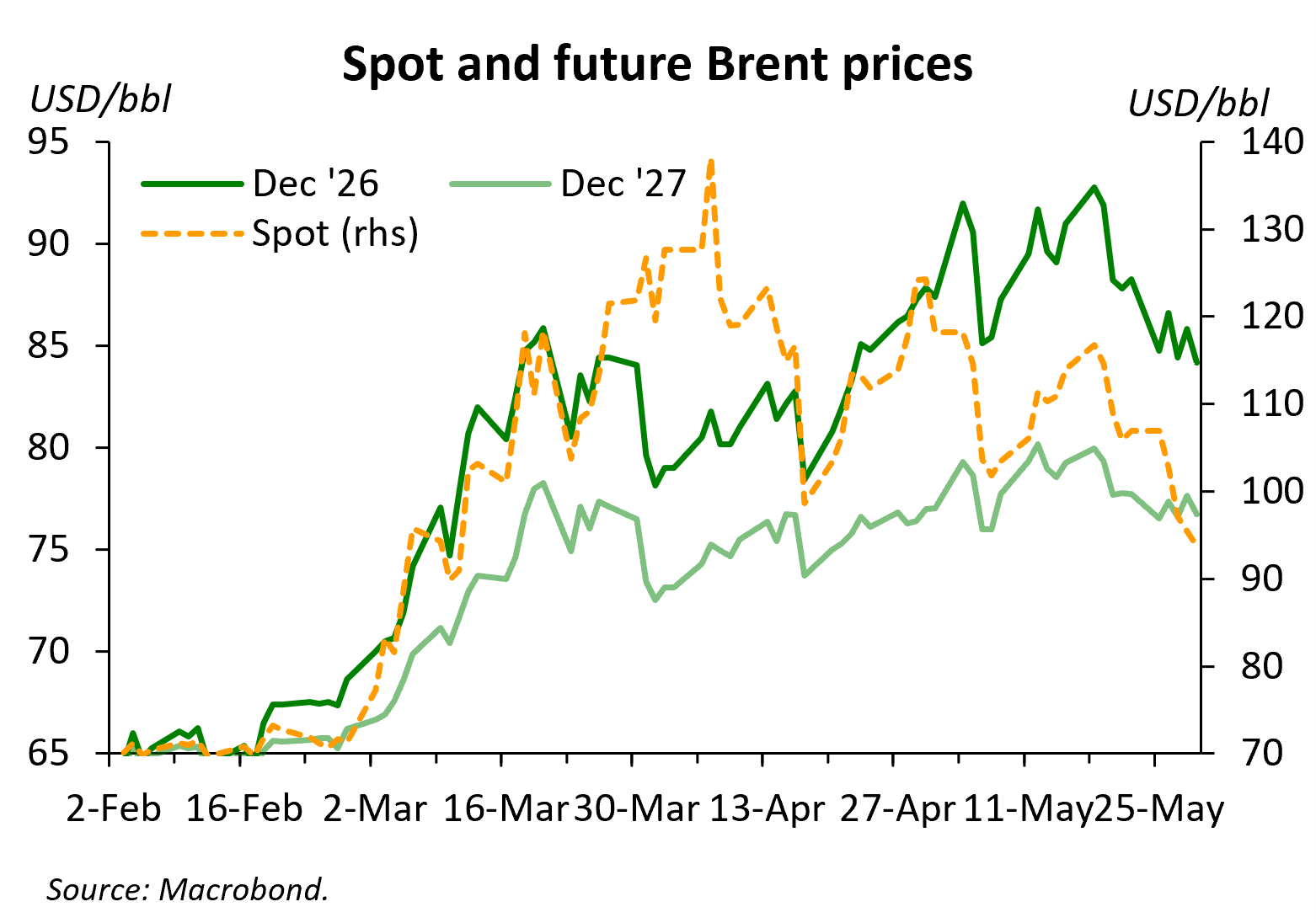

Supposing that futures prices represent a reasonable forecast for crude oil, the YoY change in oil prices can be expected to fall from about 70% currently to about 31% in Q3 before rising temporarily to about 35% in Q4. World food price inflation would appear to face some near-term upward pressure — note that rice futures have risen 15% over the past month — but perhaps we should not expect a lot of relief from moderately lower oil prices in terms of the passthrough to food prices.

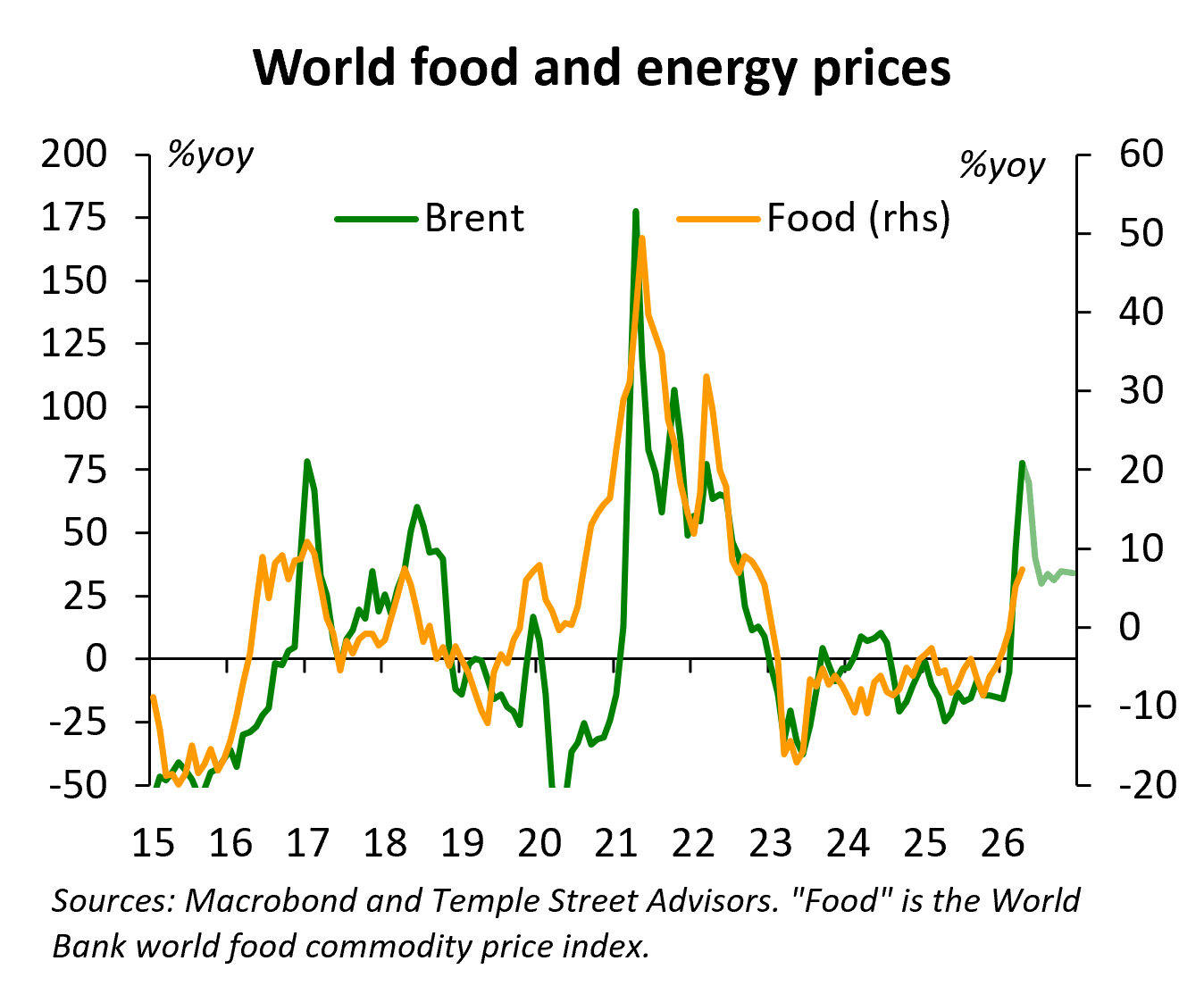

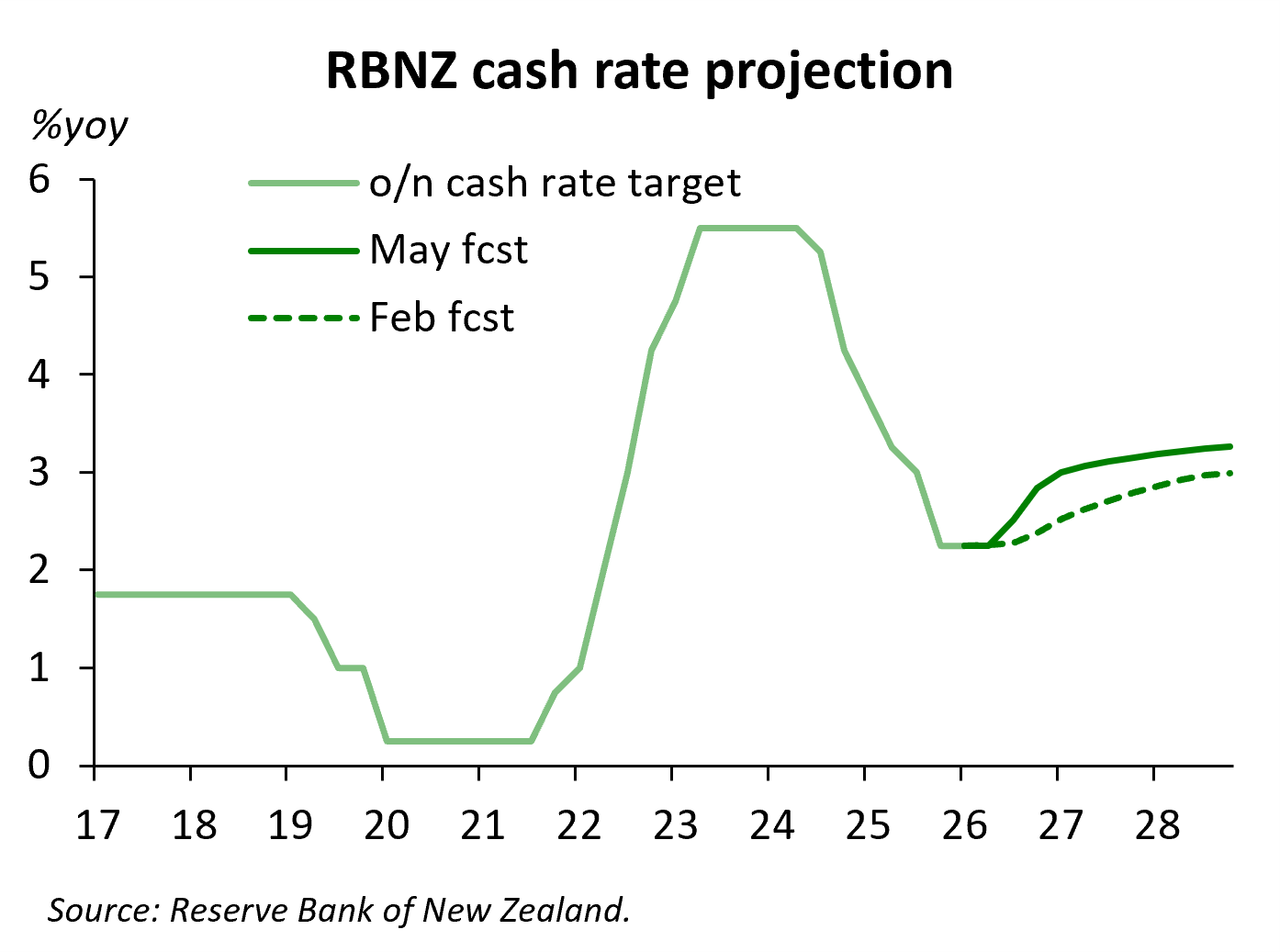

RBNZ prepares the path for rate hikes

As expected, the Reserve Bank of New Zealand did not change its policy rate last week. But it did signal that it expects to hike rates soon. The key phrase in their statement is: “On balance, the OCR will most likely need to increase sooner and by more than envisaged in the February Monetary Policy Statement.” The Bank’s inflation forecast now has inflation in Q2 rising by 1.5ppts relative to their February forecast to 4.2%. It is expected to be marginally higher (4.3%) in Q3 but falling by the end of the year. The forecast is predicated on a Dubai crude oil price of USD96/bbl at the end of the year.

The Bank also lowered its GDP growth forecast significantly, exemplifying the dilemma faced by most central banks confronted with rising inflation and slowing growth. Whereas previously they expected growth to recover to 2.8%yoy in Q4 from 1.3% at the end of last year, now they foresee growth of only 1.8%. Growth will be commensurately stronger in 2027 — rising to 3.5% in Q4 versus the previous forecast of 2.8%. So 2026 GDP growth has been revised down to 1.7% from 2.6% previously, while 2027 growth is essentially unchanged at 2.5%. The unemployment rate, which was previously expected to fall from 5.4% at the end of last year to 5.0% at the end of this year, is now expected to stay at around 5.4%.

The spike in inflation in the new forecast is largely the first-round effect of higher oil and gas prices. To contain subsequent second-round effects from firms passing on higher energy costs to consumers of non-energy products, the central bank is signalling its willingness to raise interest rates more quickly than their previous plans. They now see a 25bps rate hike coming in August, a second in November (possibly more than 25bps) and a third in February next year. Their projection has another rate hike by 2028Q3 for a total of 100bps of rate hikes.

The Committee considered alternative scenarios that mostly involved much higher inflation — approaching 6% this year — and therefore cash rates possibly rising above 4% next year. I wouldn’t be surprised if the only thing that stopped them from hiking last week was the possibility that Trump would agree to the ceasefire extension and that therefore oil prices might fall faster than they expect.

Bank of Korea on hawkish hold

The Bank of Korea, like the RBNZ, opted to keep its policy rate unchanged last week at 2.50% but the decision and the Governor’s statement to the press offered a very hawkish perspective on the outlook with a strong bias among Board members to hike rates more than once in the next six months. Indeed, two of the seven members voted to hike rates by 25bps last week — they had not dissented against the ‘hold’ decision in April.

…