Talking Points

A new global supply shock from Indonesia? BoJ Governor signals a rate hike on June 16, I think they probably shouldn't. RBI, like BoK, probably should have hiked last week.

Donald Trump has finally admitted that his ceasefire isn’t working. Firstly, it isn’t a ceasefire, just “shooting in a more moderate manner” as he puts it. Second, he’s been trying for weeks to convince us that a complete reopening of the Strait of Hormuz had all but been agreed and was imminent. Iran disagrees; and Trump can’t get what he wants without them. Having made it clear how much leverage they have over him, Iran appear to have the upper hand in the negotiations, rejecting the simple deal that Trump proposed to reopen the Strait and demanding that the ceasefire extension apply also to Israel, insisting the deal include the release of frozen Iranian funds, and refusing to discuss nuclear fuel or weapons until after the initial agreement is implemented not as a precondition to reopening.

Yet, with no end to the war in sight and hostilities increasing by the day, crude oil markets remain calm. Spot prices were up about 5% last week, still well off their highs, but December futures were up only 1.4%. The strong US jobs report on Friday was probably the biggest influence on the market — futures fell 1.2% on Friday as Fed Fund futures rose to their highest level since February 2025 with a rate hike now in the price by year-end. Since Kevin Warsh was confirmed, the December 2026 Fed Funds future rate has risen 14bps and the December 2027 rate has risen 31bps. US stocks had their worst day in eight months on Friday, dropping 2.7%. All of a sudden, rising interest rates are a problem for AI stocks — the NASDAQ dropped 4.2% on Friday, its worst day since the chaos of April 2025.

This week, I’ll discuss the new regulations in Indonesia forcing exports of key commodities to be managed by a central government SOE rather than by the exporters themselves. This regulation has very negatively impacted investor sentiment already and the stage could be getting set for a showdown between the markets and the government.

Bank of Japan Governor Ueda gave an important — and hawkish — speech last week in which he laid out reasons why the BoJ should hike rates when the Board meets on June 16. I explain below why I think they will but probably shouldn’t.

The Reserve Bank of India didn’t hike rates last week; I thought they probably would. Inflation reports in South Korea, Taiwan and Vietnam last week increase the pressure on those central banks to hike rates.

Now, let’s get into it.

Indonesia’s export control regulation

As I wrote a couple of weeks ago, investors had responded negatively to the Indonesian government’s announcement on May 20 that it would take over the external marketing of strategically important commodities. The mood has not improved as we learn more about how this will be done.

Starting with coal, palm oil and ferroalloys, with provision to review and add other commodities at three month intervals, the new regulations that took effect last Monday require that strategic export commodities must be exported by a state-owned corporation acting as owner or sole intermediary. For this role, the government has appointed Danantara Sumberdaya Indonesia (DSI), an arm of the state investment fund BPI Danantara, which is the holding company for all central government SOEs similar to Malaysia’s Khazanah or Singapore’s Temasek.

The regulation notes that: “Article 33 paragraph (3) of the 1945 Constitution of the Republic of Indonesia states that “The land and water and the natural resources contained therein are controlled by the state and used for the greatest prosperity of the people. ….. In order to realize the mandate … as long as the state has the capital, technology, and management capabilities to manage Strategic Natural Commodities, the state should directly manage them. By carrying out direct management, all the results and profits obtained will become state profits which will bring more optimal benefits for the welfare and prosperity of the people.”

Market participants and exporters can be forgiven for thinking this is a money grab. Danantara, on Friday, explained that initially they would focus on their role as an intermediary sitting between and not disrupting the relationship between exporters and their customers abroad. Their objective is “trade that is fair, transparent, and free from under-invoicing practices”.

That points to perhaps the main motivation behind this regulation: the President’s belief that under-invoicing of exports is rampant and that Indonesia is thereby robbed of its rightful magnitude of export proceeds and tax revenues. Danantara confidently states that during the transition to centralized export management, which must be completed by year-end, “Contracts that have already been signed may continue to be carried out, provided there is no under-invoicing.” How would they know? And is under-pricing a big problem?

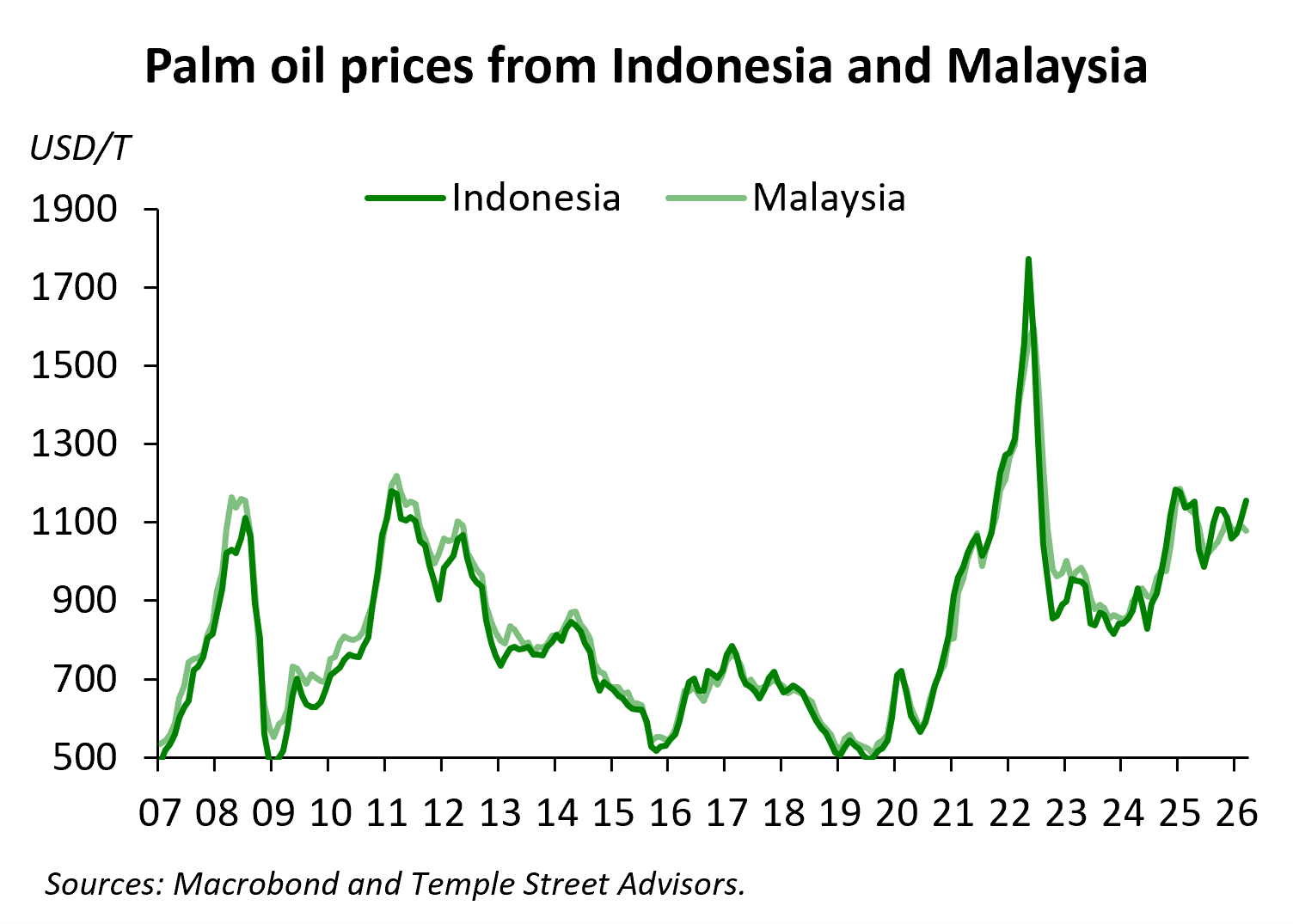

Consider palm oil, one of Indonesia’s most important commodity exports. Indonesia and Malaysia together dominate world trade in palm oil. Indonesia accounts for about half of global exports, Malaysia about one-third. It’s essentially the same product and they report export prices that are essentially the same, as you’d expect. If Indonesian exporters are under-invoicing exports in order to hide profit abroad, they must be collaborating with their Malaysian competitors very precisely.

For other commodities, direct comparisons — at least, with aggregated data — are complicated. Take coal, for example. Indonesia and Australia are the world’s two largest exporters but Indonesia exports thermal coal while Australia exports a mix of thermal and metallurgical coal. And Australia’s thermal coal has a higher energy content than Indonesia’s allowing it to command a higher price. A simple comparison of the two countries’ export prices would be misleading.

The regulation provides a transition period under which by the end of this year the exporting of strategic commodies must be done exclusively through DSI. While DSI says that they want individual exporters to maintain the relationship with foreign buyers, the regulation requires that those export prices must be set by DSI, which says it will be guided by prices on exchanges. But if there isn’t a perfect concordance between the Indonesian product and the product traded on an exchange, how will they set the price? The aim is transparency, but the process is likely to be no more transparent than the decentralised one currently in place.

But there is, perhaps, another motive for this regulation besides under-pricing. While Indonesia is one of the largest exporters globally of a number of commodities, the government perhaps believes that it doesn’t exercise market power that its size should afford it. Palm oil, for example, has a thousands of smallholders that account for about 40% of production — although they are usually reliant on the big estates to process their fruit. So at the grower level it is a very competitive business. But even at the scale of the large corporations, the government may feel that they compete too much against each other, resulting in a price-taking behavior where the government perhaps thinks Indonesia should exert some monopolistic price-setting power.

So, by centralizing the marketing of palm oil, the government may be hoping to exert more market power, pushing up the price of this extremely useful product. An ‘OPEC for palm oil’, if you will. So importing countries may face significantly higher prices for their palm oil. Except that there are provisions for exemptions from the regulation for exporters who have signed investment or domestic processing or refining undertakings with the government. So perhaps most large firms will be exempt, while the regulation will apply mainly to small domestic suppliers. In which case, the government may not achieve its goals. In the process, though, by inserting itself into the industry, DSI may accrue bargaining power over the thousands of small palm oil growers, to the latters’ disavantage.

Meanwhile, amid the confusion about how the new regulations will work, reports are emerging of smallholders exiting the palm oil trade, cutting down their trees and growing other crops for domestic sale.

This probably isn’t the last we’ll hear of this Regulation 24.

RBI keeps rates steady

As expected, the Reserve Bank of India did not change its policy rates last week. In their statement, the Monetary Policy Committee noted that the economy has not yet been especially negatively impacted by the war. Private consumption and investment have been resilient, merchandise export growth was strong in April — although ytd growth is only 1.3%yoy — and services exports have held up well. But, “While the economy has withstood the conflict spillovers with limited impact so far; the strains are increasingly becoming visible.” And the monsoon season is expected to bring lower-than-average rainfall in this El Nino year, negatively affecting demand and possibly raising inflation.

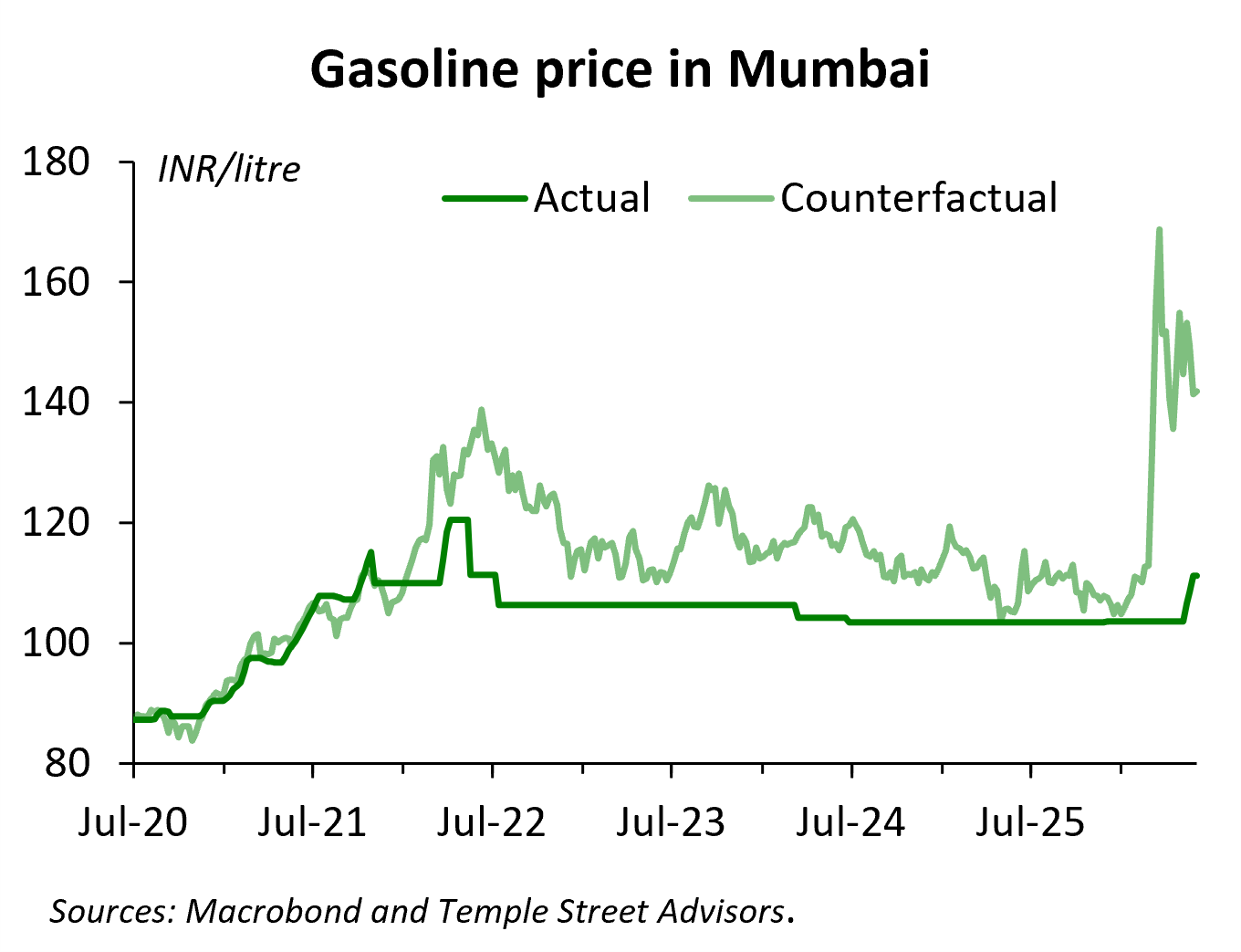

The RBI expects GDP growth of 6.6% in the fiscal year ending next March versus 7.6% in the 2025/26 year. While the government had shielded households from higher fuel prices through April, a series of price increases in May have pushed gasoline prices up 7.6% and diesel prices up 8.6%. This will directly increase the inflation rate (3.5% in April) by 0.36%. Indian firms already pay higher prices for imported petroleum and derivative products and these price increases are expected to be at least partially passed on to consumers. So inflation is expected to rise to about 5.9% in Q4 this (calendar) year before easing slightly in Q1 next year.

I’d expected the RBI to hike by 25bps to get ahead of rising inflation expectations as consumer fuel prices are now rising and businesses have been dealt higher input costs that they may try to pass on in the context of still-strong growth in consumer spending. The depreciation of the INR — down 6.1%ytd versus the USD, not a calamity but compounding the rising import prices — is another reason to hike. But with inflation below the mid-point of the RBI’s target range, policymakers do have room to monitor inflation for a while to see how much the higher fuel prices are passed on to consumers. They appear willing to continue with foreign exchange market intervention to try to prop up the INR rather than trying to make the currency more attractive in terms of yield.

My expectation is that retail prices for gasoline and diesel will continue to rise gradually. The government has not provided any guidance on how high prices will go other than to say further increases can’t be ruled out. Even after last month’s price increases, the oil companies are losing about INR35 per litre of gasoline sold and about INR18 per litre of diesel — a combined daily loss of about USD57mn. I estimate that to return to the previous (positive) margins earned by the oil companies — and if the government plans to reverse the INR10/litre excise tax cut made at the end of March — retail gasoline prices would have to rise about 28% even if crude oil prices in INR terms don’t rise from here.

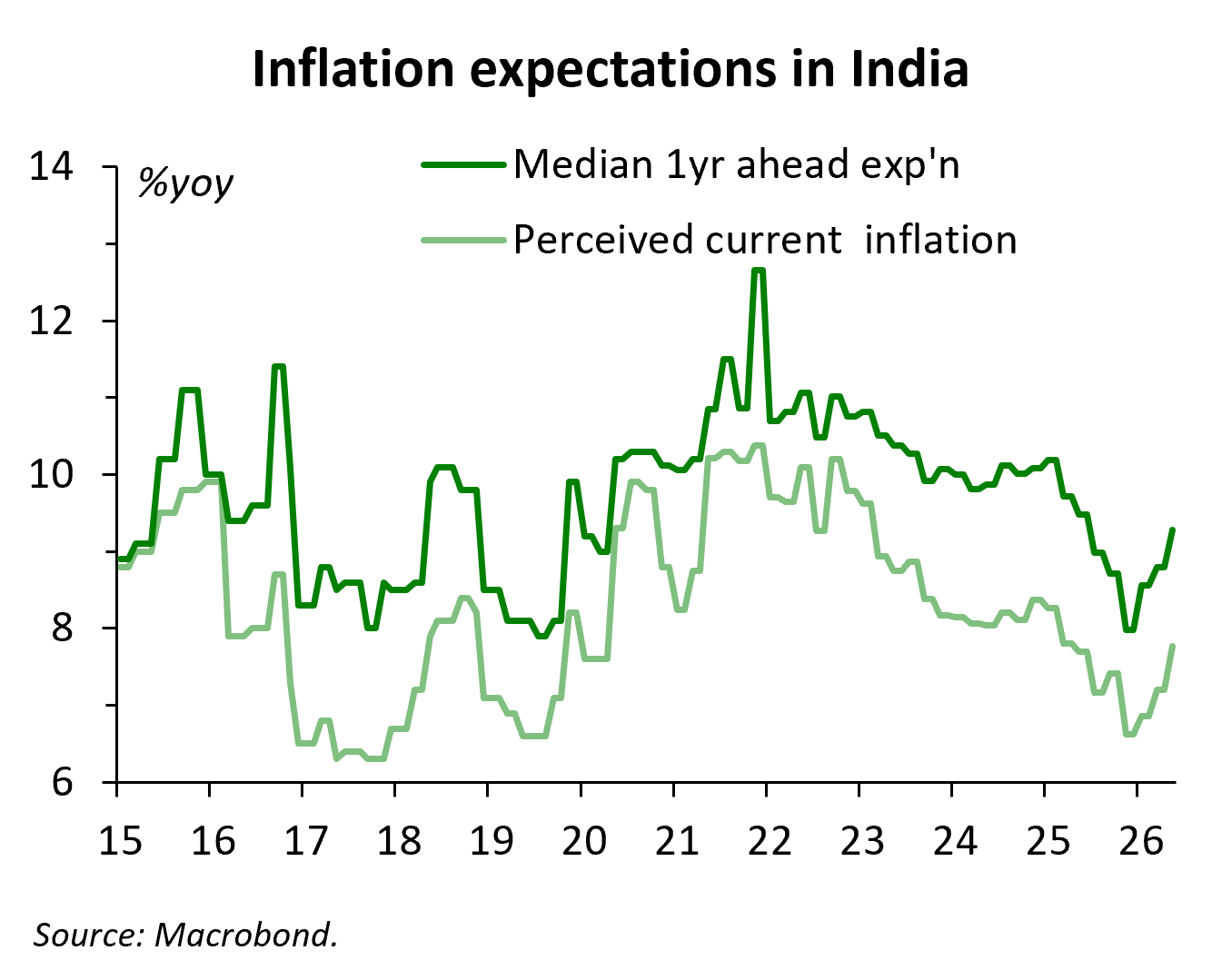

According to the RBI’s surveys, inflation expectations in India are rising, although given the subdued rate of inflation over the past year, expectations are not particularly high. Households generally perceive inflation to be higher than it actually is — a common phenomenon — and almost always expect inflation a year ahead to be about 1.5ppts higher than the current rate. But year-ahead inflation expectations are at a one-year high and rose sharply in May when retail fuel prices were raised.

So if inflation expectations are already rising and fuel price increases have only just begun, a rate hike last week would have been defensible. But perhaps not urgently needed. But if the stalemate in the Gulf continues, or the war heats up, and oil prices start rising again, I’d expect the RBI will hike rates before summer’s over.

BoJ Governor signals a hike on June 16

Bank of Japan Governor Ueda sounded a notably — for him — hawkish tone in his speech at the Kisaragi-kai meeting last Wednesday. The key phrase in his speech was: “Japan is currently in a situation in which the secondary spillover effects of inflation stemming from higher crude oil prices are more likely to lead to an upward deviation in underlying inflation. The Bank considers that it is necessary to make decisions about future policy based on this premise.”

He quickly rejected the argument that a central bank should not hike rates in response to a temporary supply shock, arguing that this shock is likely to prove long-lasting and therefore more likely to lead to significant passthrough to non-energy prices; that consumers’ and firms’ behavior has changed in a way that reinforces this risk; and that despite raising the policy rate from -0.1% to 0.75% over the past two years, financial conditions have actually eased — due to lower (negative) real rates and rising equity valuations. Hence, he argues, the central bank needs to tighten policy notwithstanding the potential downside risks to growth from the war.

Where you stand on the BoJ’s view comes down to how you read the following chart. It is a variant of the Phillips Curve, using the GDP output gap instead of unemployment (which changes very slowly and very little in Japan) plotted against a measure of underlying inflation (I explain below exactly how this measure of inflation is calculated).

Keep reading with a 7-day free trial

Subscribe to The Asia Economist to keep reading this post and get 7 days of free access to the full post archives.