Talking Points

Your 10-minute briefing on APAC macro and markets. APAC equities continue to outperform the US this year. Whose inflation expectations should matter for policy? PBoC and RBI get good inflation data.

It was a very good week for investors in APAC equities — especially North Asian equities, which have been outperforming ASEAN and the US for most of the year. Bond yields continued to decline in most markets, despite talk of bond market vigilantes pushing yields higher.

The Fed is almost certain to cut rates this week, but the data released last week on inflation (rising but no more than expected) and inflation expectations (rising more than expected) should give them more pause. The risk is we get a ‘hawkish cut’ this week with the Fed pushing back against the more bullish market forecasts for rates.

Inflation reports from China — rising but at a moderate pace — and India — returning towards the mid-point of the target band — suggest not need for either central bank to change monetary policy.

North Asia stocks continue to outperform the US

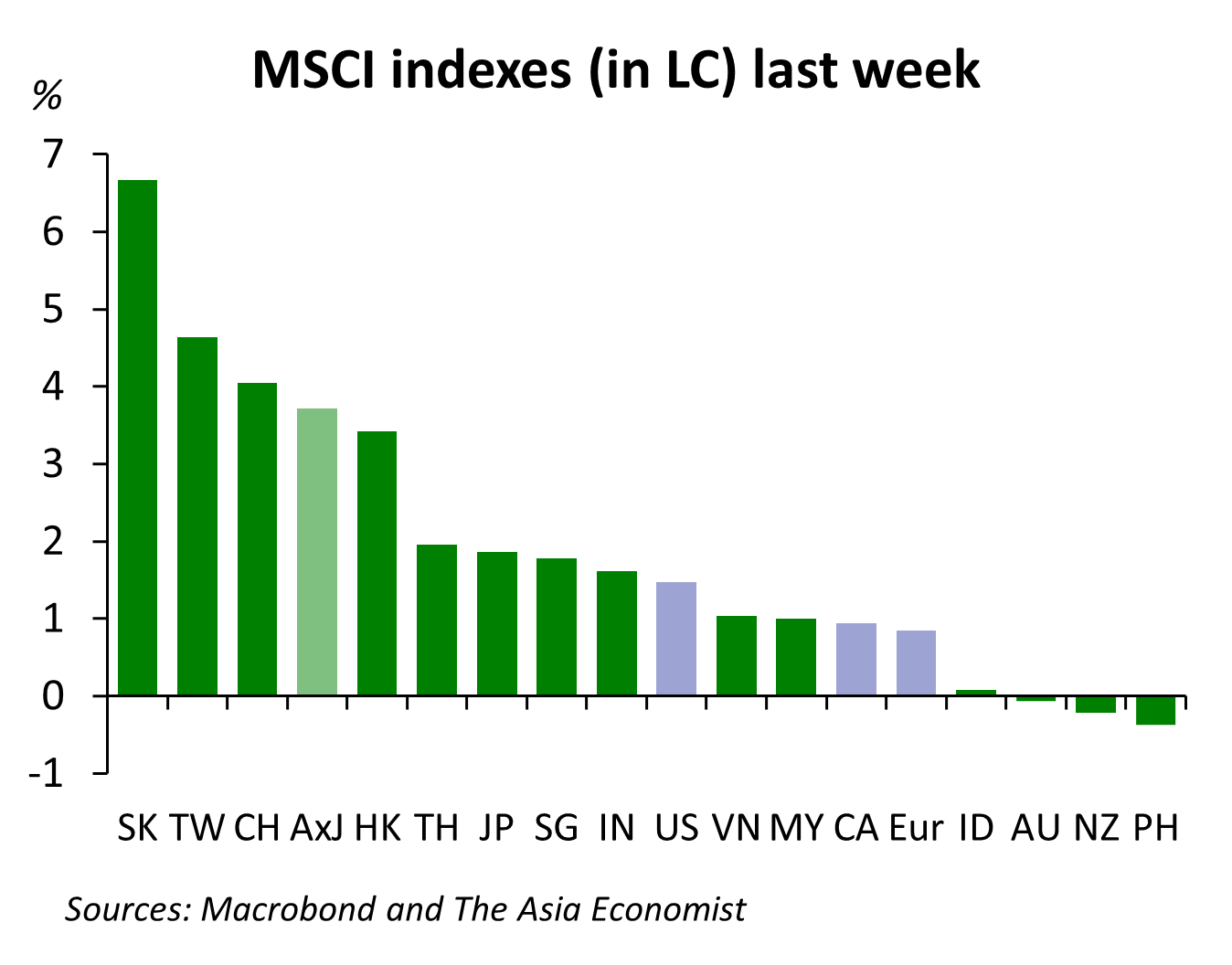

Last week was a good week to be invested in US equities, but it was an even better week to be invested in Asian equities. US stocks rose 1.5% last week, but the MSCI Asia ex-Japan index rose 3.7%. Adding the effect of generally stronger currencies, the total return on the Asia ex-Japan index was 4.2% last week. This was the best week for that index since late September in the wake of the China stimulus announcement that saw the Chinese market rise 17% in four days. Once again, the South Korean market led the way last week, gaining 6.7%. Taiwan and China gained more than 4%, while Hong Kong rose 3.4%. Markets in Australia, New Zealand and the Philippines fell slightly — less than 1% — while the Indonesian market eked out a 0.1% rise.

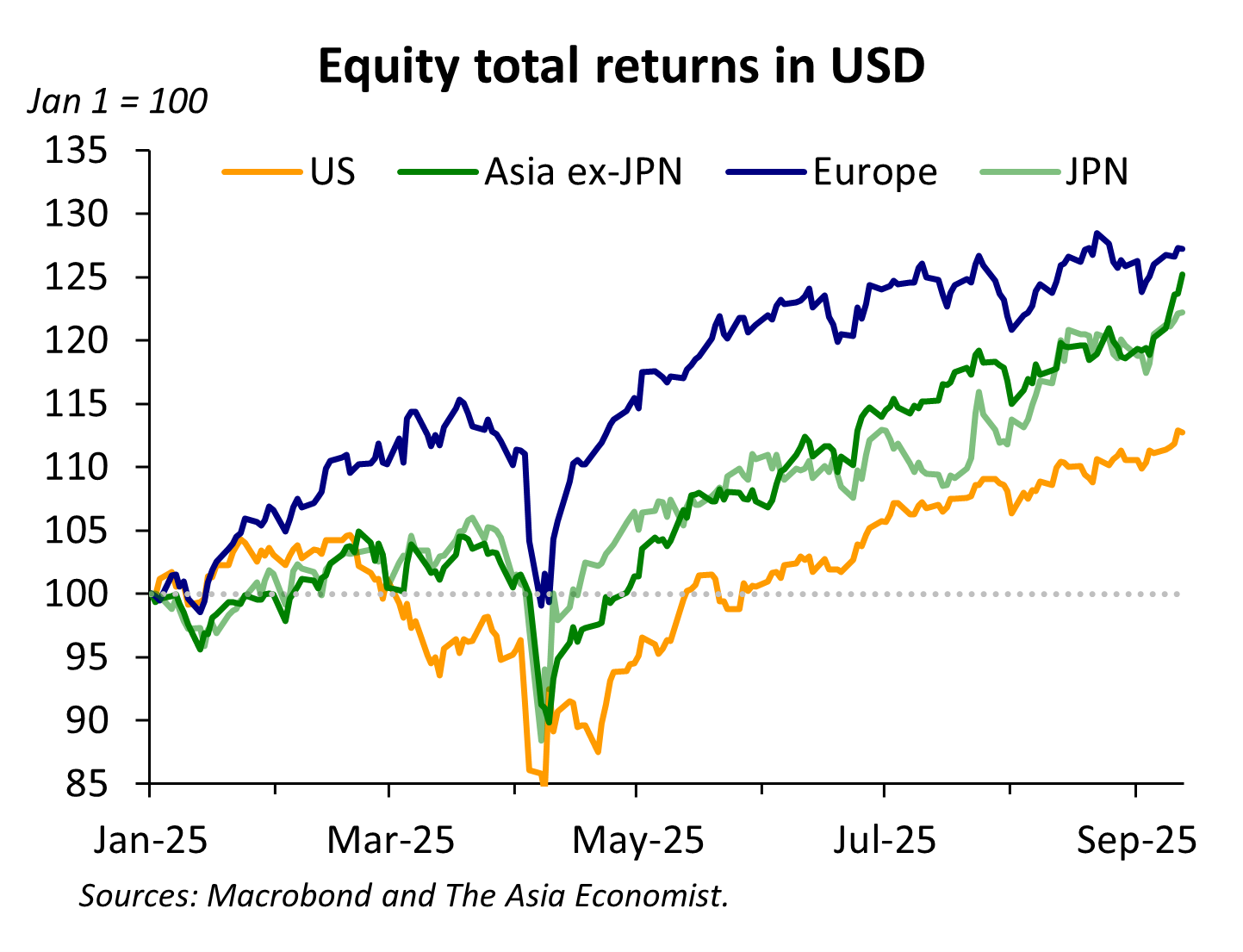

Year-to-date, while US stocks have returned a credible 12.8%, the Asia ex-Japan index is up 25.4%, and Japanese stocks have returned 22.2% in dollars. European stocks continue to lead the regional leagues, with a dollar return of 27.2%ytd, but they have underperformed since July.

The outperformance of Asian and European stocks versus the US market this year comes down to two factors. First, tariff announcements have been more negative for the US than for the countries hit with tariffs. After President Trump began to apply tariffs in February, starting with a 10% levy on imports from China announced on February 4, the US market dropped 8% over the following five weeks while stocks in the other regions posted small gains — amplified by dollar weakness. Then the April 2 ‘reciprocal’ tariff announcement resulted in a 12% drop in US equities over the next four days, worse than the declines in other regions. Second, the dollar has depreciated against most currencies this year, augmenting the returns to foreign stock holdings for dollar-based investors.

In fact, since the announcement on April 9 that those April 2 tariffs had been scaled back to 10% to allow for negotiations and until September 5, the four regions had actually delivered very similar returns. The total return on the Asia ex-Japan index, in USD terms, was essentially the same as the 32% return on US stocks. Japanese stocks delivered a 28% return while European stocks delivered 24%.

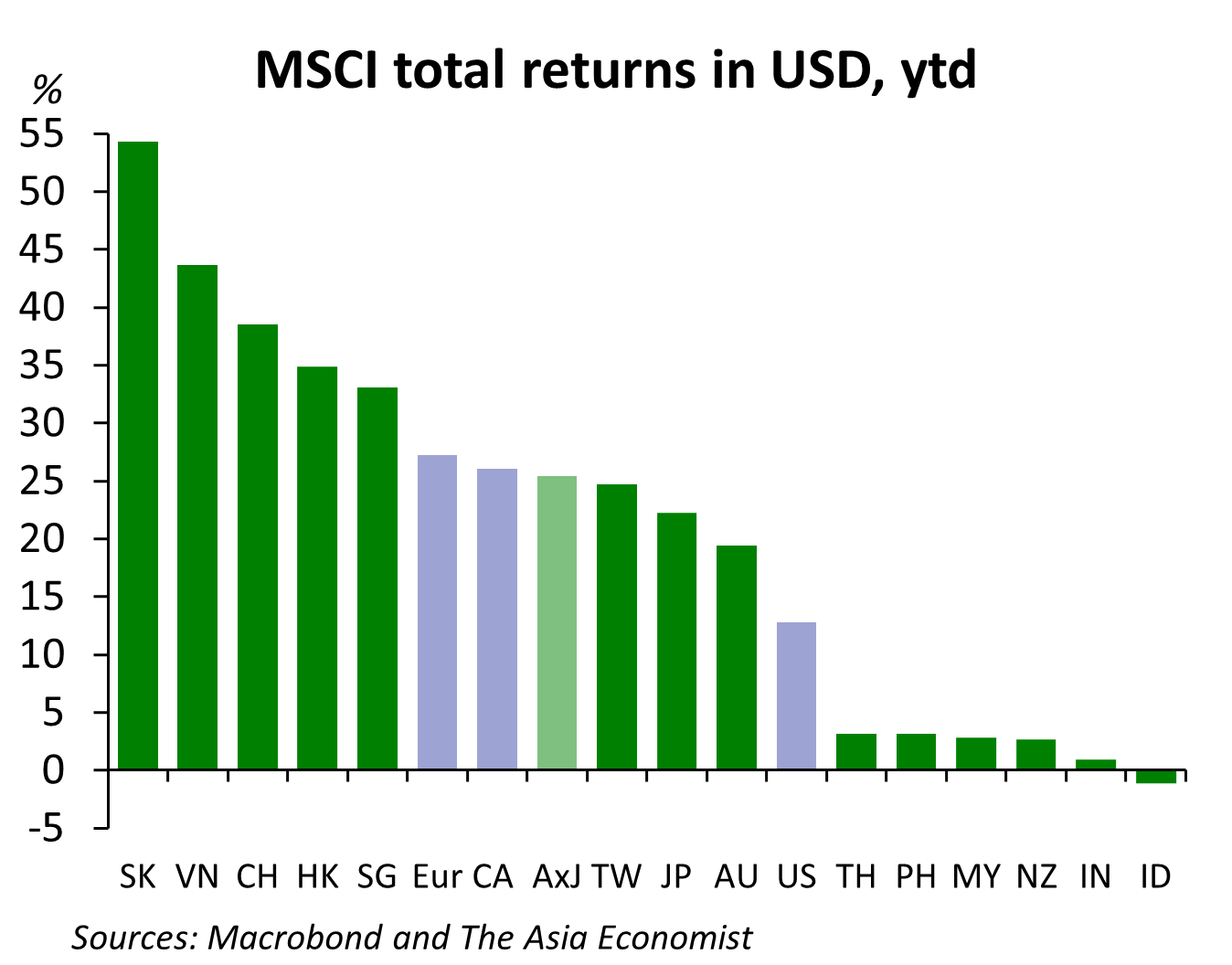

But within the Asia Pacific region, there’s been a great divergence between North Asian stocks and most ASEAN markets and New Zealand. The Indonesian market has delivered a slightly negative total return in dollars this year — less than 1% in IDR terms, even. It had been a laggard even before the recent protests. Total returns to USD investors in Thailand, the Philippines, Malaysia, and New Zealand have been only about 3%, while Indian stocks have delivered 1% in dollars.

By contrast, as I’ve noted almost every week, it has been a fabulous year for investors in South Korea (54%ytd in USD), Vietnam (44%), China (39%), Hong Kong (35%) and Singapore (33%). Stocks in Taiwan, Japan and Australia have delivered better than 20%ytd returns, on average double the return in the US market but lagging Europe and Canada.

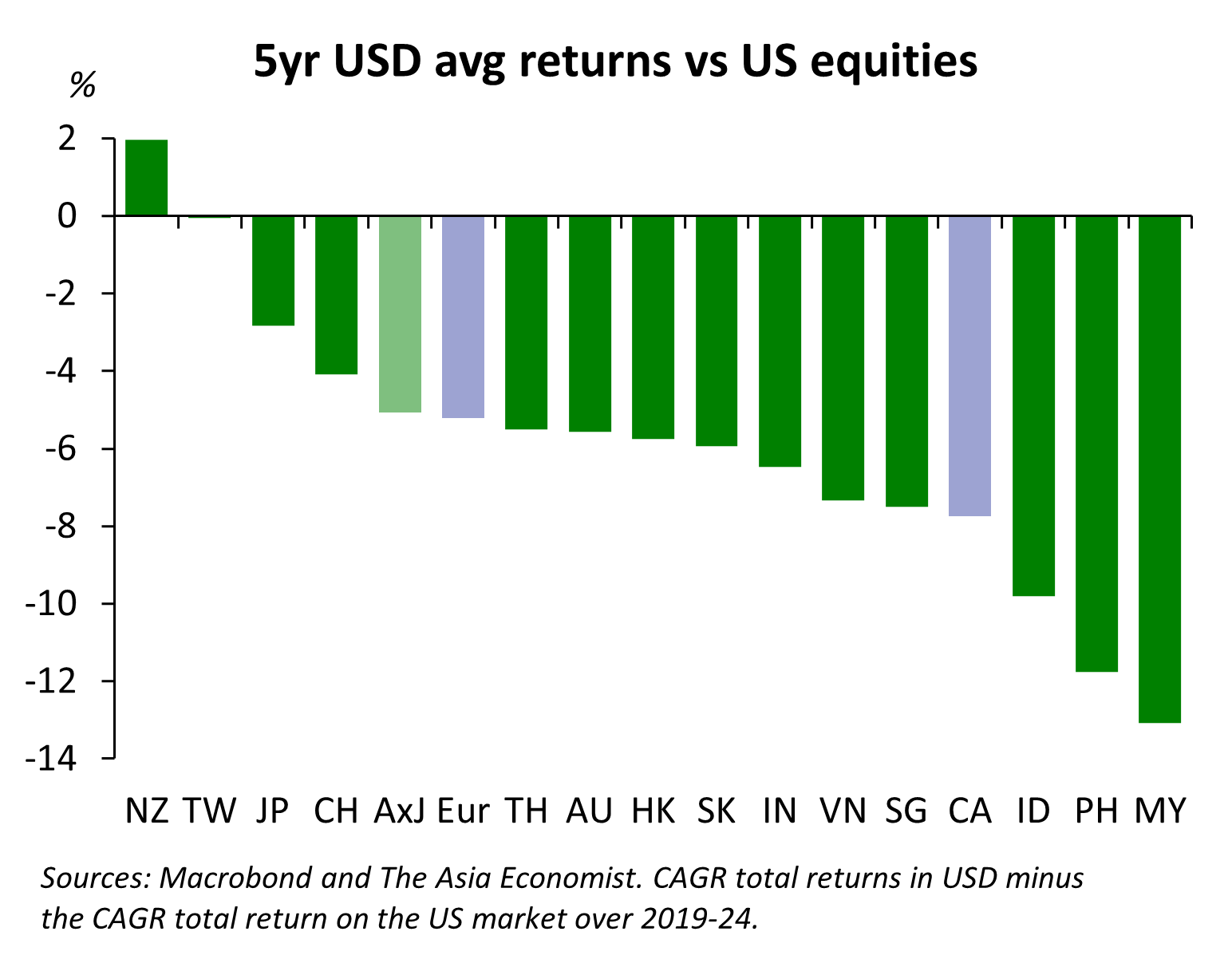

Before we get too congratulatory about the Asia Pacific region, though, remember this this year’s outperformance comes after many years of relatively poor returns. Over the five years of 2020 through 2024 — the pandemic years and recovery — only New Zealand, by a slim margin, delivered a higher CAGR of USD returns than the US. Malaysia, the Philippines and Indonesia, which have significantly underperformed the US this year had also significantly underperformed over the previous five years.

The fact that ASEAN stocks except Vietnam continue to underperform, by a considerable margin, the North Asia markets is, I think revealing. One of the aims of Trump’s tariffs is to reduce the US’ reliance on Asian supply chains, especially for IT goods. So, he incentivizes Apple, TSMC and Samsung and others to move production to the US from Asia. While companies in Japan, South Korea and Taiwan will remain dominant players in the IT space in Asia Pacific even if they move production to the US, the ASEAN countries’ role as production nodes is being undermined. They, and to some extent India, had hoped that a “China +1” strategy for multinationals would leave them room to continue to expand manufacturing. But Trump’s tariffs undermine such a strategy — the “+1” will be the US.

Vietnam is vulnerable to the same logic. While the ‘reciprocal’ tariffs create an incentive for Chinese firms to export to the US via Vietnam — a 40% ‘penalty’ tariff is lower than the average tariff on goods imported directly from China — this loophole could easily be closed. Chinese-owned factories in Vietnam, as is the case with Chinese-owned firms in the UK, should expect to be hit with the China tariff.

Bonds rally despite “vigilante” claims

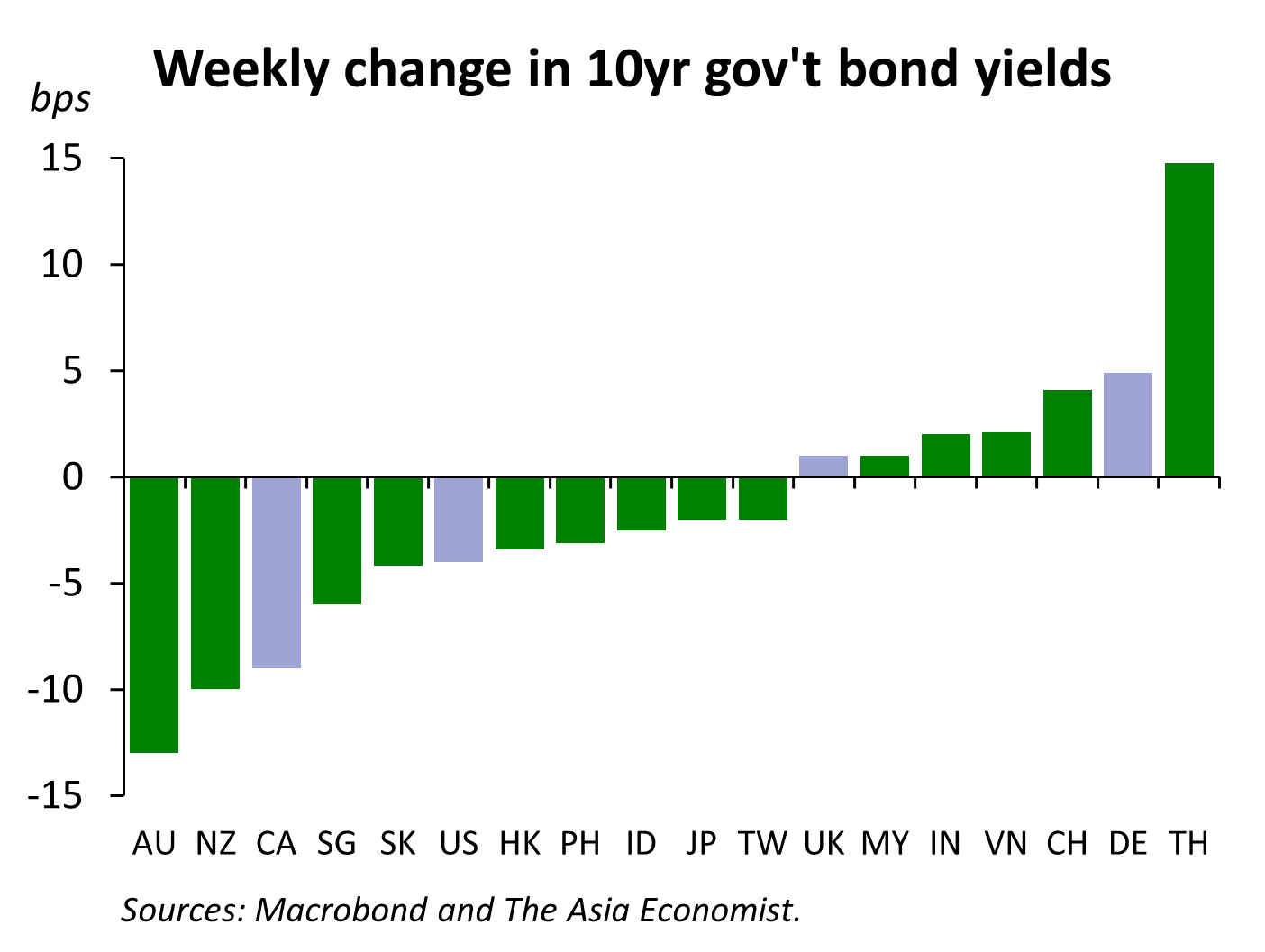

Financial markets commentary in recent weeks has focused more on the bond market than the equity market. More and more, analysts are talking up the risks of a government debt crisis due to high levels of debt and deficits. The FT (here) and Bloomberg are not alone in reviving the old “bond vigilantes” spectre. Except that even as they wrote these words, bond yields have been falling. The US 10yr yield fell only 4bps last week, but it had fallen 13bps the previous week and 27bps over the past month. The yield on Thursday — 4.01% at close — was the lowest since April 4.

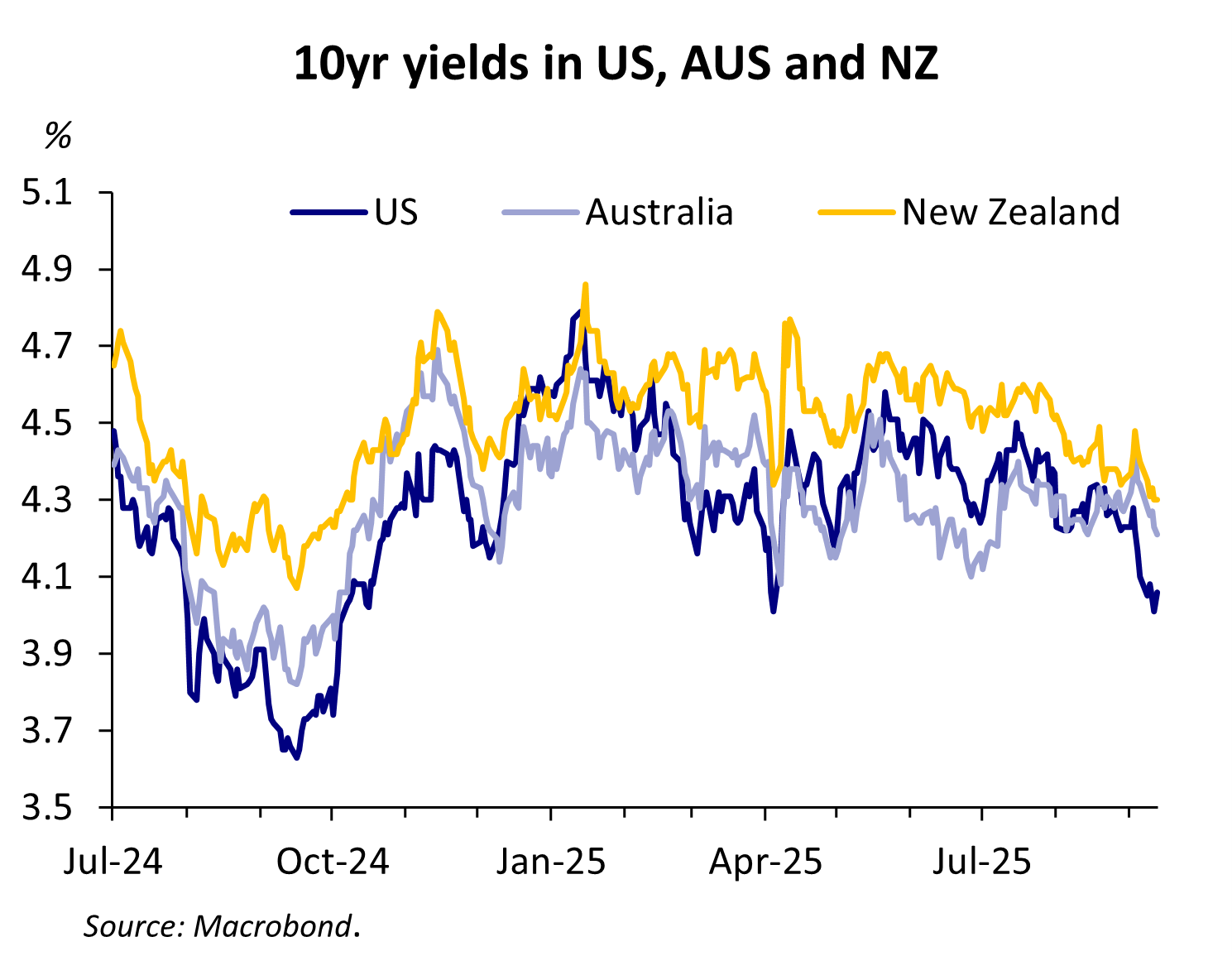

Most APAC markets saw lower bond yields last week, but only in Australia and New Zealand were the moves significant. Both of these markets historically track US yields closely — open capital accounts with no central bank intervention helps, so the move lower largely reflects the movement in US yields. Australian yields have actually been notably more modest as better-than-expected data in recent weeks has pushed out the timing of rate cuts.

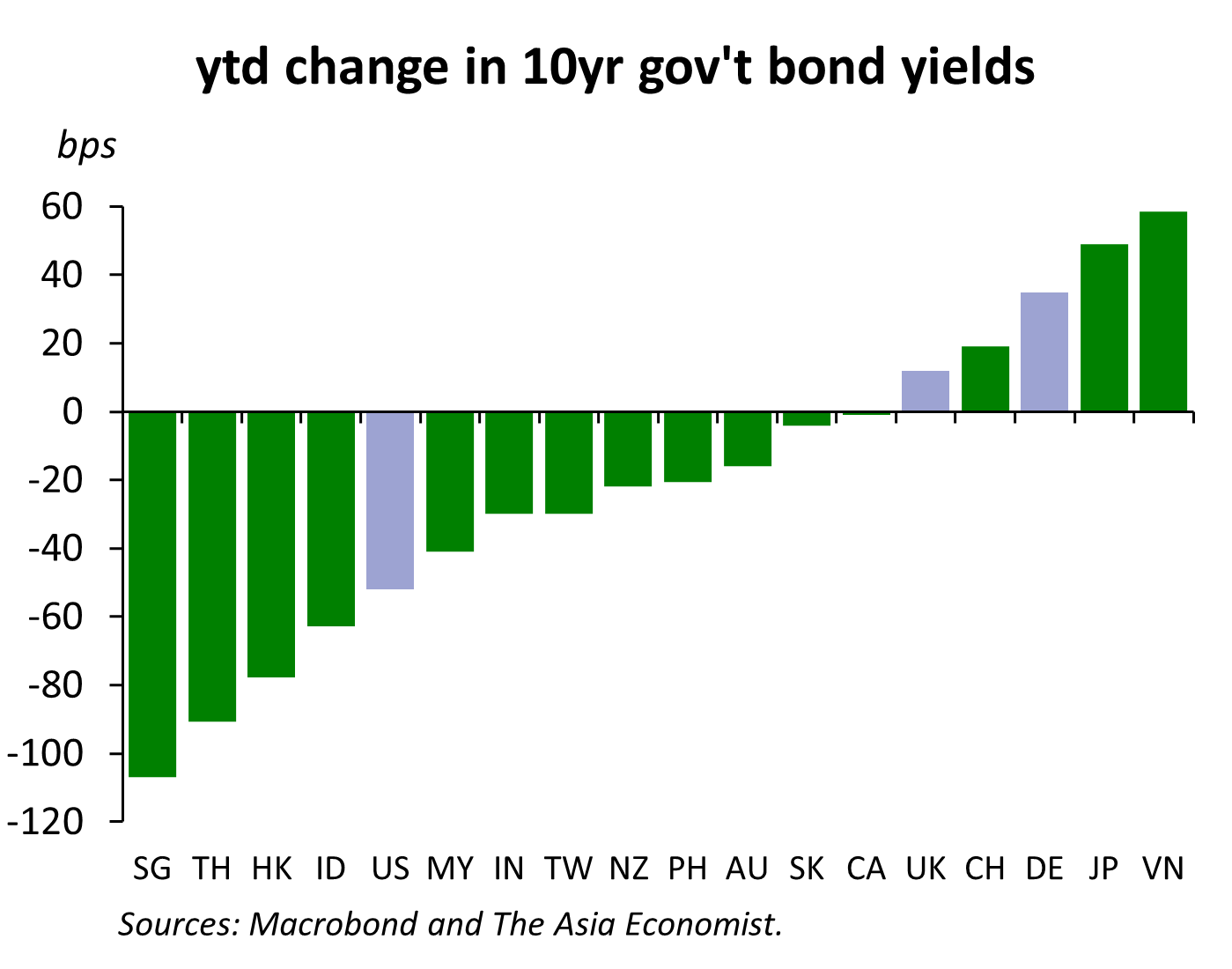

Year-to-date, US 10yr yields have fallen more than 50bps while yields in Singapore and Thailand have fallen about 100bps — even after a large 15bps backup in Thai yields last week. The bond vigilantes may be selling 30yr bonds — although I have my doubts that fiscal discipline is what’s at work there — but they don’t seem worried about the 10yr outlook.

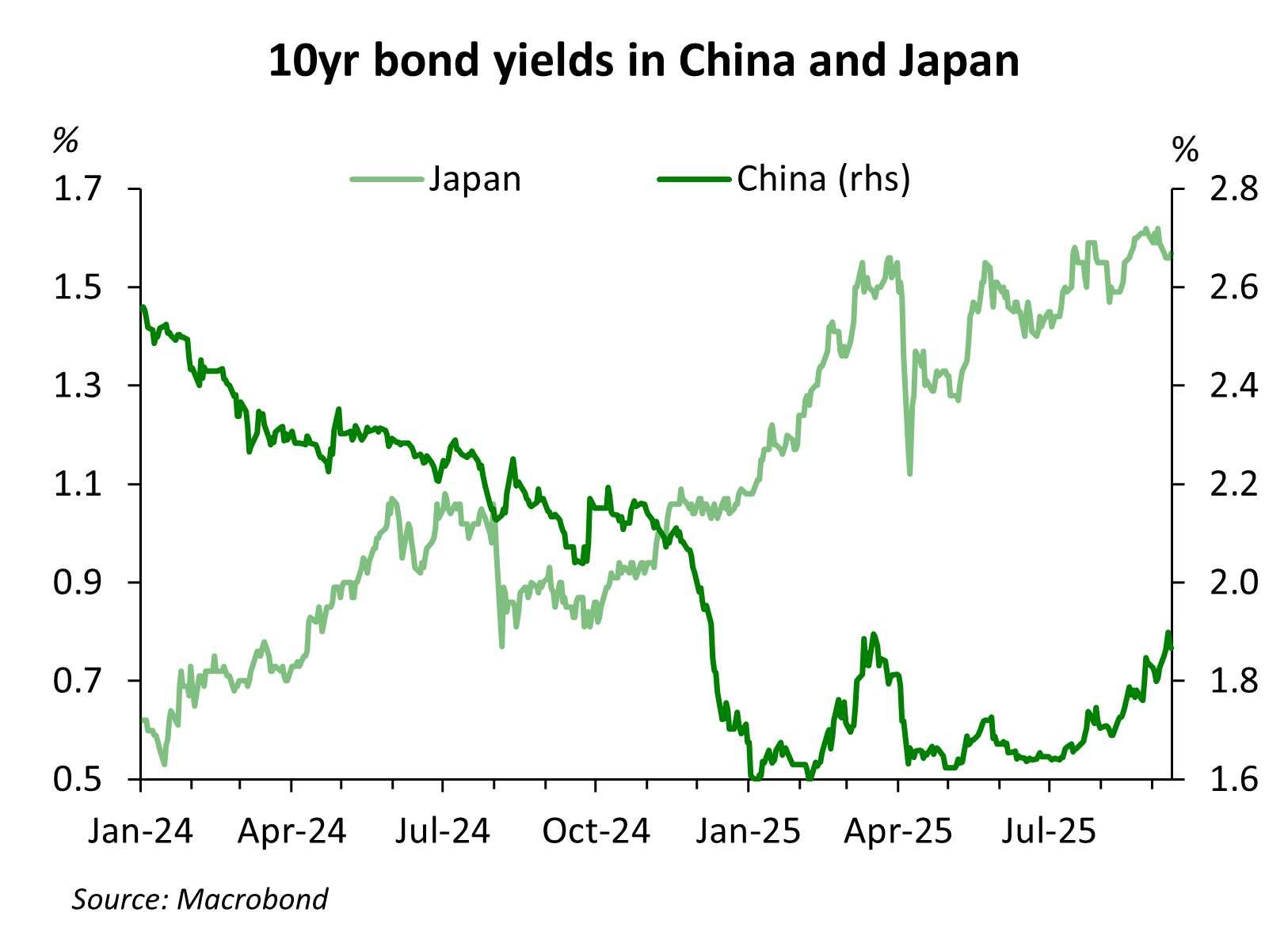

The most interesting markets where yields are rising are China and Japan. Both are reflation stories. Chinese yields plunged late last year partly out of concern for tariffs and what they’d do to the growth outlook but mainly, I think, because investors thought the People’s Bank of China had embarked on a QE program and they wanted to get in front of that. The PBoC had said they wanted to build up their portfolio of bonds to expand their toolkit for managing liquidity. As their holdings nearly doubled in the second half of last year, investors thought that was just the beginning of the purchases. Instead, the PBoC stopped buying in January — their government bond holdings have fallen by 20% — and with core inflation continuing to rise the deflation threat, and chances of more rate cuts, is receding.

In Japan, the pause on monetary tightening caused by the tariff threat has perhaps gone — although you can never be sure with Trump, which is his tactic — but inflation appears to have peaked. The Bank of Japan is stuck in a dilemma of its own making — arguing that underlying inflation is really very low but nonetheless that it should continue raising interest rates. It’s a mess, frankly, and the political uncertainty doesn’t help. A minority government would probably prefer the central bank wasn’t raising interest rates unnecessarily, although the US administration is again pressuring the Japanese to strengthen the yen, which rate hikes might contribute to.

(As an aside, in my August 31 note “What now?” in response to the US Federal Appeals Court decision upholding the judgement that Trump’s use of IEEPA to impose ‘reciprocal’ tariffs was illegal, I argued that even if the Supreme Court agreed with this interpretation of law, there were other ways Trump could try to achieve his goal of eliminating the US trade deficit. Weakening the USD is one of them.)

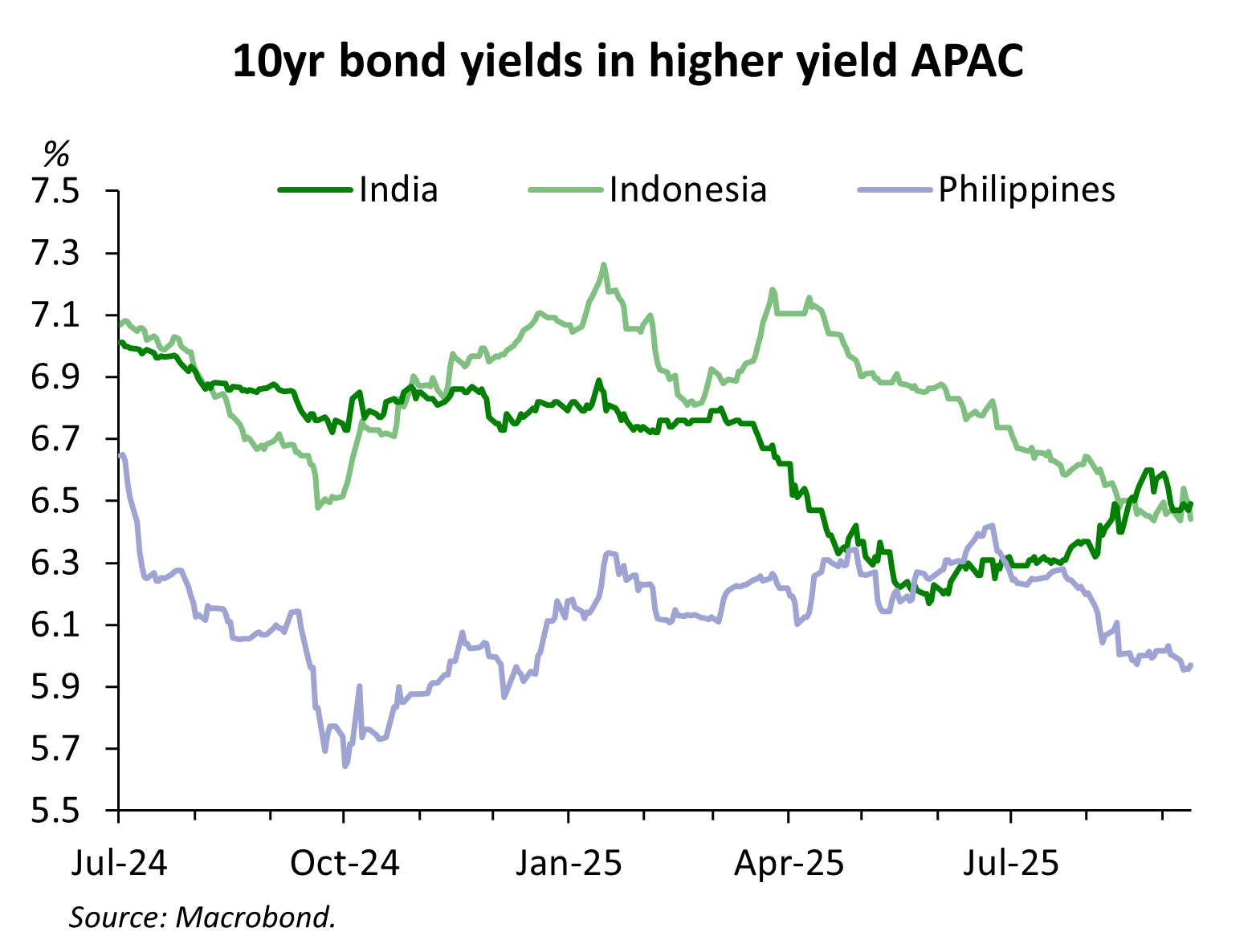

Among the high-yielding markets, bond yields in Indonesia and the Philippines have been trending down for at least the last couple of months (closer to five months for Indonesia) while Indian yields have been rising since late May.

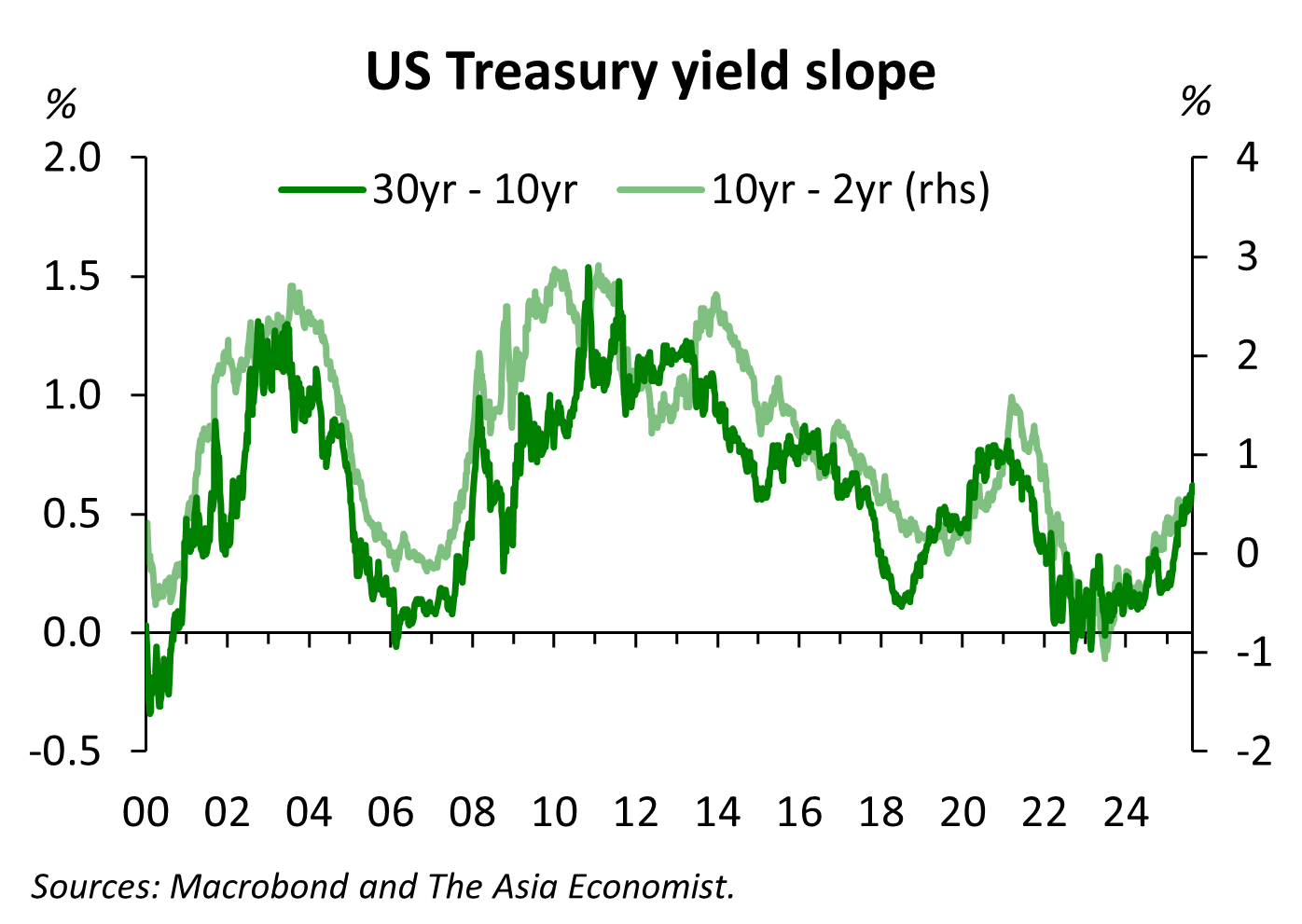

And what of the ‘bond vigilantes’ argument? The 30yr - 10yr premium has indeed risen sharply in recent months. But so has the 10yr - 2yr spread, as is normal in an environment when the Fed is, or is expected to be, cutting rates. I’m not convinced there’s anything more going on.

Most APAC currencies continue to strengthen vs USD

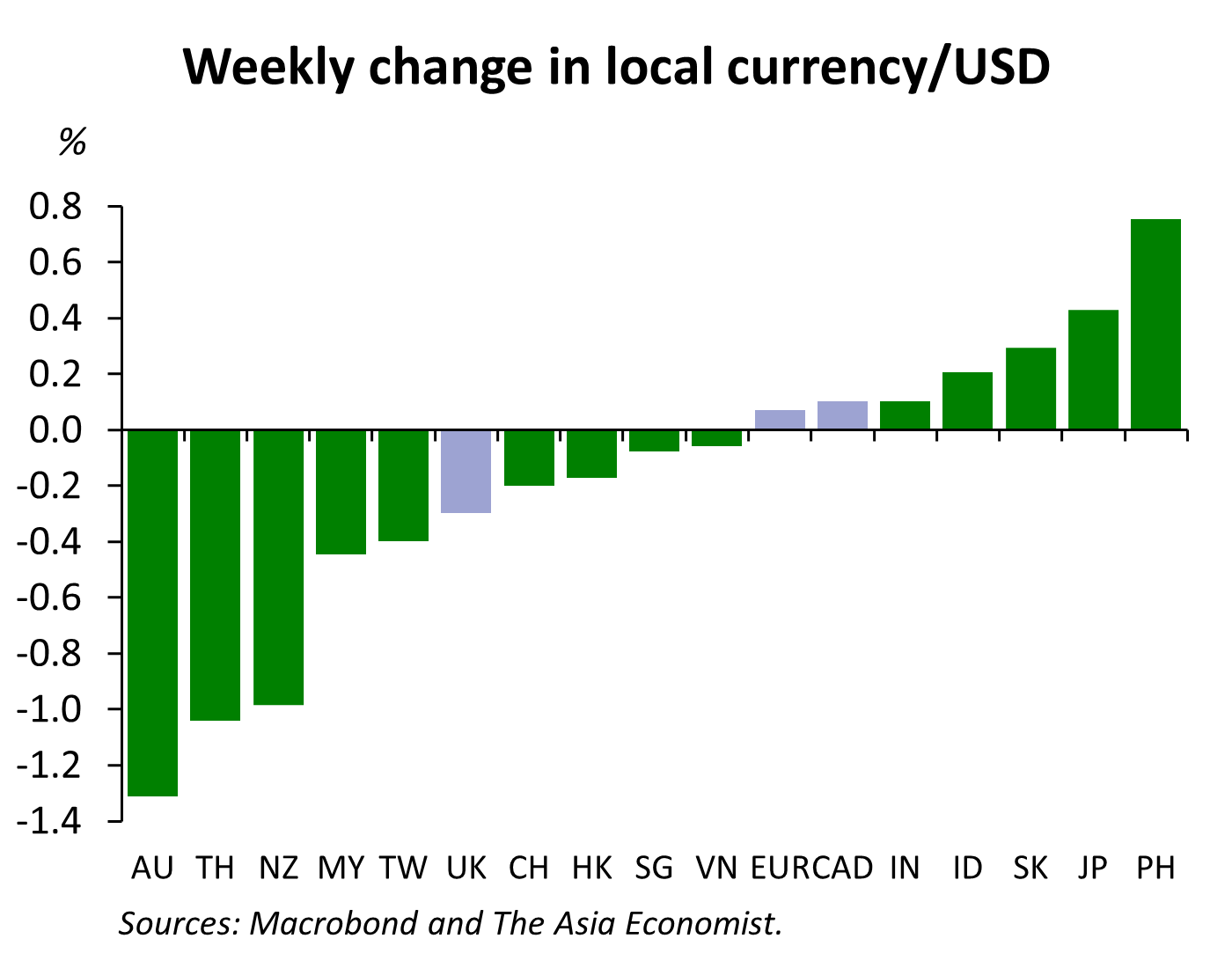

Last week again saw most currencies appreciate versus the USD — led by the AUD, THB and NZD. For some currencies — the CNY, JPY in particular — there’s a reasonably close relationship between relative interest rates and the dollar exchange rate. But that model of currency determination is less useful elsewhere. In Thailand, for example, while there was an outsized rise in bond yields last week, that came on Friday while the big move in the currency was on Monday. The AUD and NZD appreciated last week despite having bond yields that fell more than the Treasury yield.

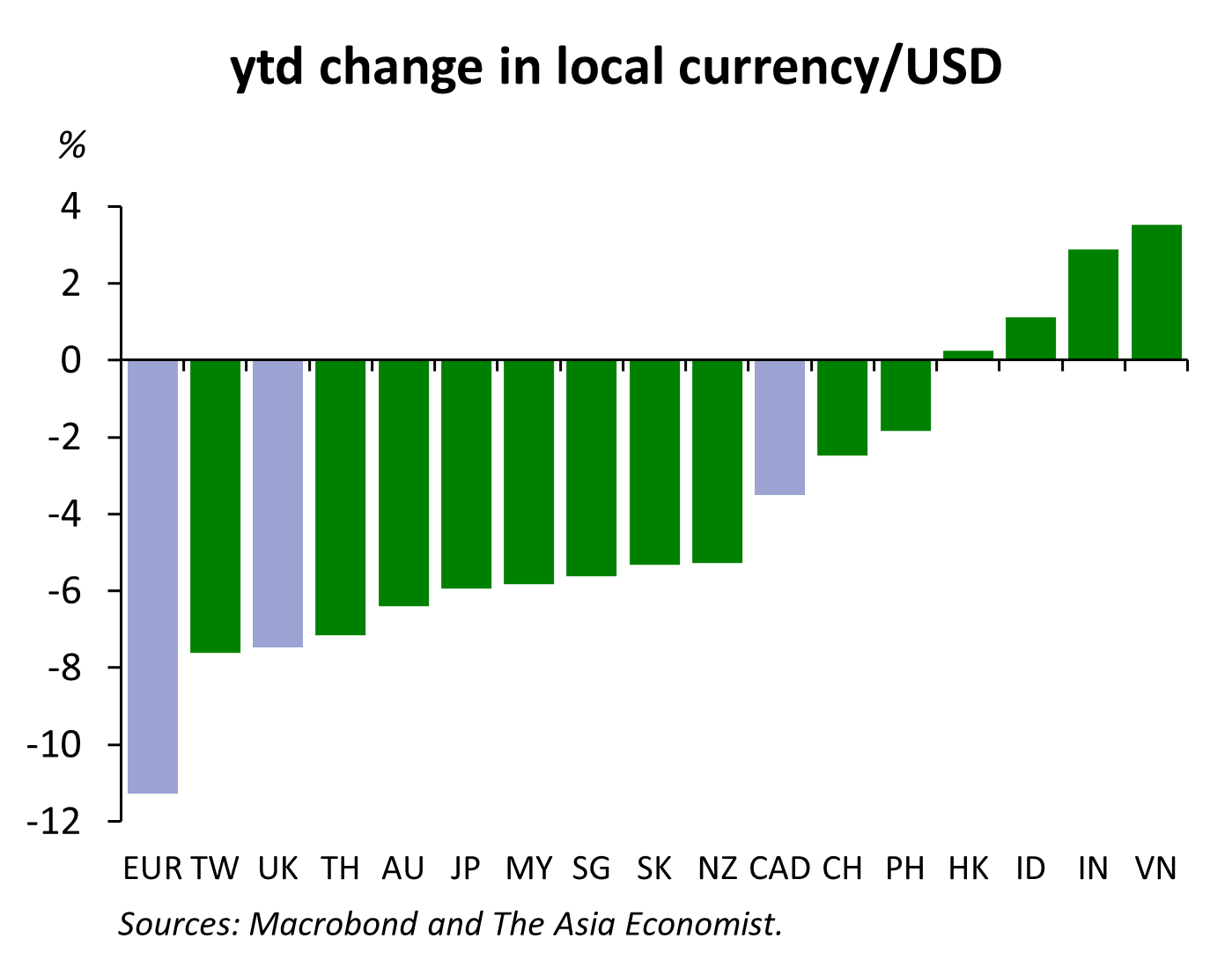

Year-to-date, the Euro remains the strongest currency in the set of currencies we care about in this publication. But almost all APAC currencies have appreciated modestly against the dollar. The VND is a managed float which always depreciates; the IDR and INR likewise have been depreciating pretty consistently for the past 14 years and the rates of depreciation for most of this year have been relatively modest.

Whose inflation expectations should matter to the central bank?

Data releases last week raise an interesting dilemma for central banks. In his Jackson Hole speech last month, Fed Chair Powell said “Measures of longer-term inflation expectations, however, as reflected in market- and survey-based measures, appear to remain well anchored and consistent with our longer-run inflation objective of 2 percent.” I beg to differ. First, though, to give him his due, market measures of inflation expectations are well behaved, at least recently, but perhaps not “consistent with” 2% inflation.