Talking Points

Trump in Beijing offers respite to Iran perhaps, and maybe even some "wins" on trade.

President Trump has rejected the latest proposals from Iran for ending the war — proposals that still look like maximal demands from a government that seems to think it has the upper hand. By all accounts, Trump wants the war to end but Iran won’t concede on Trump’s main objective of eliminating their nuclear weapons capability. I don’t expect this breakdown of negotiations to lead to a resumption of hostilities — beyond the skirmishes we’ve seen over the past week in the Strait of Hormuz — as long as Trump is in Beijing. So, as markets priced in a lessening of the threat of a reopening of the war last week, oil prices dropped and equities (and bonds) rallied. More of the same could be in store this week. But after that, who knows?

Trump - Xi summit in Beijing

President Trump will travel to Beijing to meet President Xi on May 14-15, for a summit that was originally scheduled in March but was postponed due to the war with Iran. There are, of course, a vast number of issues that could be — should be — discussed during this summit. This is the most consequential relationship in the world. But the focus of attention will likely be on the trade relationship, the war in Iran and the US policy towards Taiwan.

On trade, we are half way through the one year truce, if we can call it that, on the US - China trade war. The deal reached between the US and China in Busan last November 1, provided for a one-year pause on some tariffs and export controls. According to the White House, the Chinese side agreed to, among others:

Suspend all retaliatory tariffs and non-tariff measures (including expansion of the unreliable entities list) announced since March 2025;

End the flow of fentanyl to the US and of its precursor chemicals and certain other chemicals to North America;

Suspend the global implementation of export controls on rare earths and related measures that had been announced in October 2025 and issue general licenses for the export of rare earths, gallium, germanium, antimony, and graphite for the benefit of U.S. end users worldwide;

Extend the expiration of its market-based tariff exclusion process for imports from the United States and exclusions until December 2026;

Terminate anti-trust and other regulatory investigations on US companies involved in the semiconductor supply chain;

Suspend the actions taken in retaliation for the US Section 301 investigation on China’s Targeting the Maritime, Logistics, and Shipbuilding Sectors for Dominance.

Purchase 11mmT of US soybeans by end-2025 and 25mmT of soybeans in each of 2026, 2027 and 2028.

The US, in turn, agreed to:

Lower the ‘fentanyl’ tariff on China to 10% and maintain the 10% ‘reciprocal’ tariff rate until November 10, 2026;

Extend the expiration of certain Section 301 tariff exclusions until November 10, 2026;

Suspend until November November 10, 2026 the application of the “Expansion of End-User Controls to Cover Affiliates of Certain Listed Entities” that had been announce in September 2025;

Suspend until November 10, 2026, implementation of the actions taken in following the Section 301 investigation on China’s Targeting the Maritime, Logistics, and Shipbuilding Sectors for Dominance.

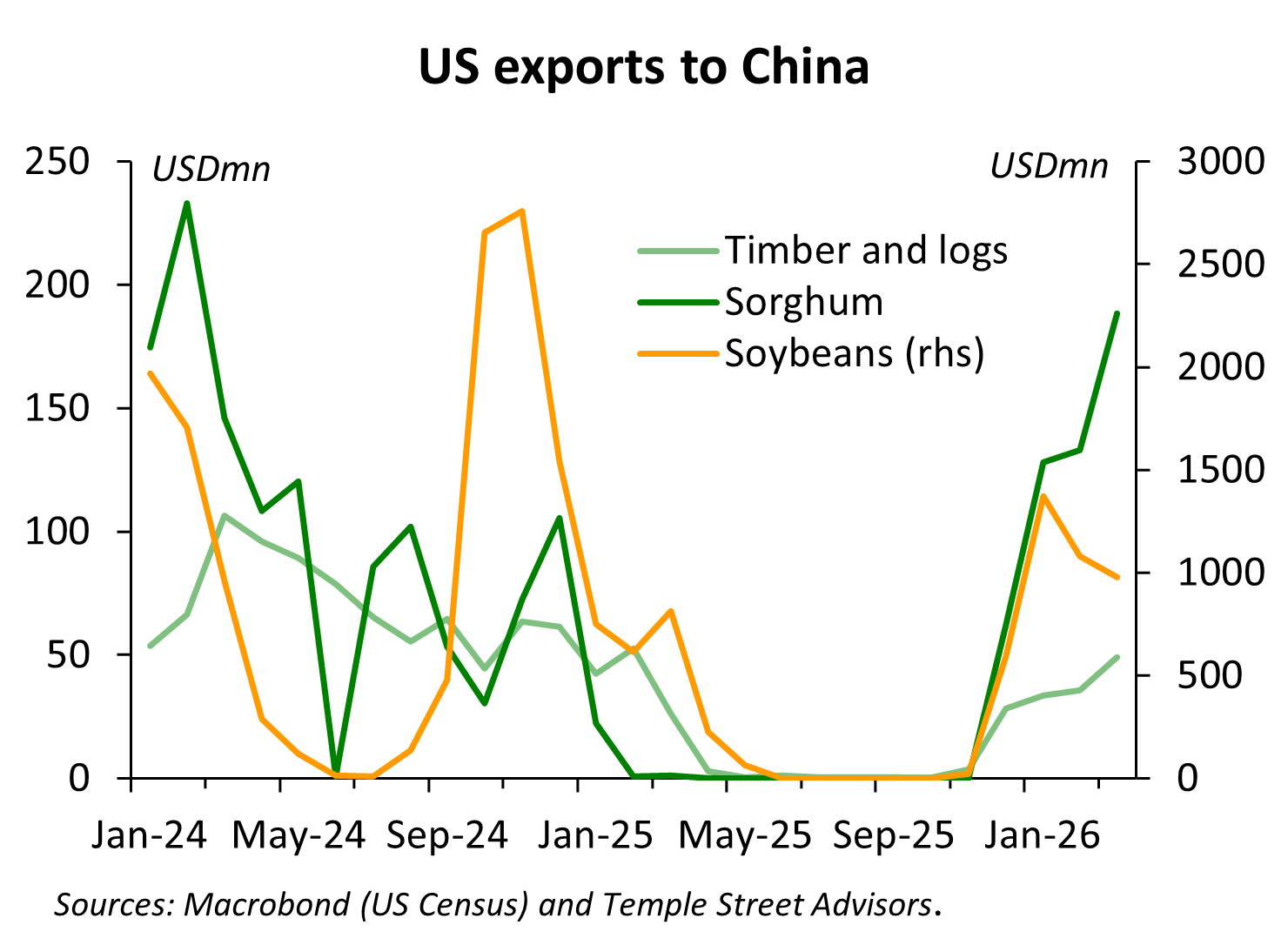

The tariff and other administrative measures are easily verifiable. As for purchases of agricultural goods, after having fallen to essentially zero by May of last year, US exports of soybeans, sorghum and lumber — the three products explicitly mentioned in the deal, started rising in November. Soybean exports are running at an average monthly pace of 2.1mmT since November, consistent with the commitment made.

So, unlike the Phase One deal in January 2020 that was scuppered by Covid, China appears to be living up to its commitments made last November. However, imports of agricultural commodities other than soybeans, sorghum and timber were at at least a 15-year low last year. So perhaps this week we’ll see Trump demand that China increase imports of corn, rice, wheat, beef etc. Meanwhile there’s lots of speculation that Xi will commit China to buying 500-600 Boeing aircraft valued at about USD100bn based on list prices.

If Xi Jinping can get Trump to focus on ‘wins’ like commitments to buy more American goods, he might thereby be able to divert attention from more fundamental and structural problems such as the undervalued CNY, intellectual property rights theft, subsidies and other aspects of industrial policy, etc. That would be a win for Xi.

Both sides might want to get the other to further ease up restrictions on trade in sensitive products. The US would want China to commit to further relaxing — and for longer — export controls on rare earths, while China would want the same for US controls on sales of semiconductors and semiconductor manufacturing and designing technology. Any progress on this front would be an important and positive outcome from these talks and would send a more positive signal about the relationship between the two countries than an agreement on a shopping list.

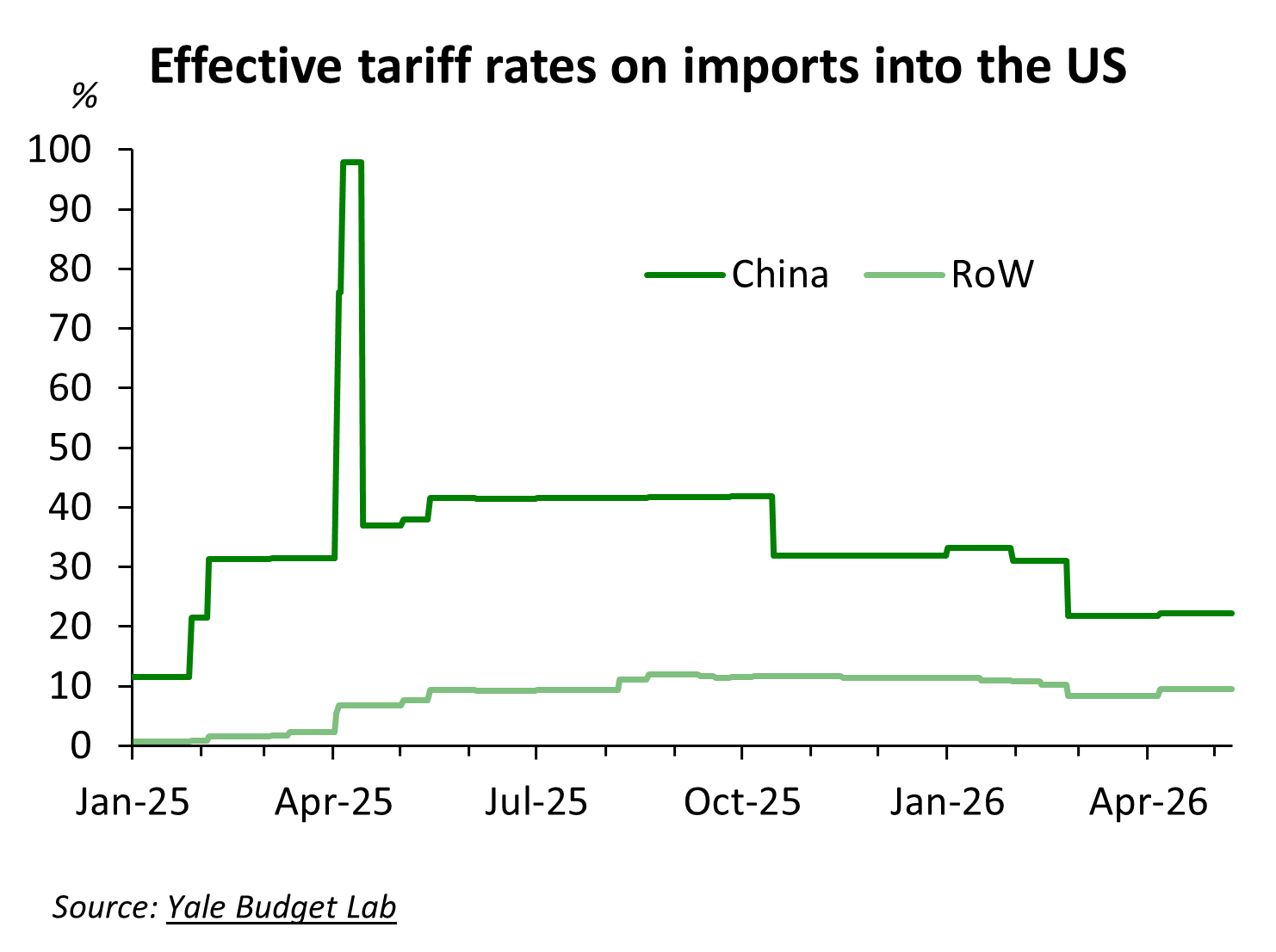

But overall, trade may be becoming less of an irritant — at least, from the Chinese side. After the Supreme Court struck down the IEEPA tariffs (the Court of International Trade struck down the Sec 122 tariffs last week but they remain in effect pending an appeal of that decision), and after Trump backed off his threats of very high tariffs on imports from China, the effective tariff on imports from China is now about 22% versus 9% for the rest of the world. That’s still a wide gap, but last summer the gap was 42% vs 9%. As long as this truce in the trade war continues — and maybe Trump and Xi agree already this week to extend it beyond November — tariffs are perhaps an acceptable cost of doing business with the US.

Which leaves strategic issues as perhaps the area where the leaders will spend more time talking. With Trump’s ceasefire in Iran faltering — the two sides continue to take pot-shots (“love taps”) at each other — and Iran not showing any sign of giving in to US demands, Trump may ask Xi to stop supporting Iran. I doubt he’ll get very far. The war in Ukraine will likely get lip service — both sides support an end to the war, but neither is willing to do anything to promote it. China supports Russia and the US has lost interest in supporting Ukraine.

Taiwan will, as usual, likely get the lion’s share of attention. Xi will ask, again, that the US make clear that it is opposed to Taiwan independence. The current US policy is that they do not support it, which is not as forceful as the Chinese side would like. The US will likely say that China’s shows of force around Taiwan — and its claims to large parts of the South China Sea and the East China Sea are a source of regional tension. Xi will counter that the US’ web of alliances and its ‘freedom of navigation’ transits are a bigger threat to regional stability. But Trump wants Xi’s help to arrange a summit with North Korea’s Kim Jong Un, so he will likely avoid pushing to hard against China on these issues.

The relationship is too important for this summit to fail to produce any progress. Both leaders want to be able to demonstrate that they can work with the other, that the relationship is improving and that they are making progress on the issues that divide them. In addition to Xi’s shopping list, we’re likely to see at least more clarity on Trump’s Board of Trade idea, a technical working group that would continue discussions on trade issues, and perhaps also a Board of Investment to do the same for cross-border investments. The latter is something the Chinese side has reportedly asked for.

Asia Pacific’s export recovery is broadening

Now that we have the Q1 trade data for all Asia Pacific economies, we can highlight the most interesting recent development.

Keep reading with a 7-day free trial

Subscribe to The Asia Economist to keep reading this post and get 7 days of free access to the full post archives.