Talking Points

Takaichi's gamble pays off with a supermajority. Expect the Takaichi trade to push yields higher and the currency weaker -- in Korea too. India's trade deals send a positive signal to investors.

Well that was interesting! All doom and gloom mid-week as stocks fell but euphoria on Friday as markets rebounded. But keep things in context. From peak-to-trough last week, US stocks were down only about 2% and ended marginally up on the week and less than 1% below an all-time high that was reached only eight trading days ago. Asia ex-Japan hit a new all-time high six sessions ago while Japan reached a new high on Friday ahead of this weekend’s election.

This wasn’t just a profit-taking correction, though. There was a clear theme last week — indeed, since the beginning of the year. Hardware trumps software. The S&P hardware index rose 5% last week and is up 13%ytd. Software fell 7% last week and is down 15%ytd. The surging investment in ‘compute’ is fueling a realization that a lot of software may become obsolete quickly as people prompt their AI tool of choice to do what they currently pay some other software provider to do.

Prominent among the software losers, though, is crypto. Bitcoin fell 16% last week (at one point it was down about 25%) and has fallen 45% from its all-time high set last October. The total value of all crypto coins issued is down 48% from its peak. It’s not just that investors are once again questioning the investment thesis behind crypto; the gold rush in AI development is sucking financial and human capital resources out of crypto.

For Asia, though, a hardware-over-software thesis plays to the region’s advantage. Friday’s rebound in US and European equities should see Asian markets start the week on a strong footing. Especially in Japan.

Japanese Prime Minister Takaichi’s election gamble has paid off. The latest — not yet final — results give her LDP and coalition partner Japan Innovation Party at least 311 of the 465 Lower House seats. The LDP alone added about 90 seats and now has more than half of the seats. But by winning a two-thirds super-majority the coalition can override a veto in the Upper House where they don’t have a majority.

The election win solidifies support for Takaichi’s fiscal stimulus — one of her key campaign pledges was to cut the consumption tax on food for two years. She has also pledged to increase defense spending to 2% of GDP this year. A staunch conservative in the mold of Abe Shinzo, Takaichi may use her supermajority to amend the constitution to remove the prohibition on maintaining a regular armed force. She has also spoken of her desire to visit the Yasukuni Shrine. Immigration emerged as a significant issue in the campaign and while she says she recognizes the value of tourism and foreign workers in Japan, Takaichi has pledged to tighten immigration rules, review rules on land ownership by foreigners and crack down on alleged non-payment of taxes or national health insurance premiums. The number of foreign workers in Japan has risen by about one-quarter over the past two years to just over 2.5mn last year.

Equities love Takaichi’s pro-growth policies, bonds not so much. The “Takaichi trade” since her election as LDP leader in October has been long equities short bonds and short the yen. That’s likely to be how Monday plays out.

Slightly lost in the noise about markets last week, Tariff Man was again back in the news with two new tariffs being levied — related to Cuba and Iran — and tariffs on India and Argentine beef being lowered. The US-India trade deal was announced last Saturday — and provided a good positive boost to markets on Monday — but only published on Friday. A week earlier, India had concluded negotiations on a free trade agreement with the EU. These two deals cover about 24% of Indian trade, so this was a milestone week for Indian trade policy. I’ll dig into these agreements below.

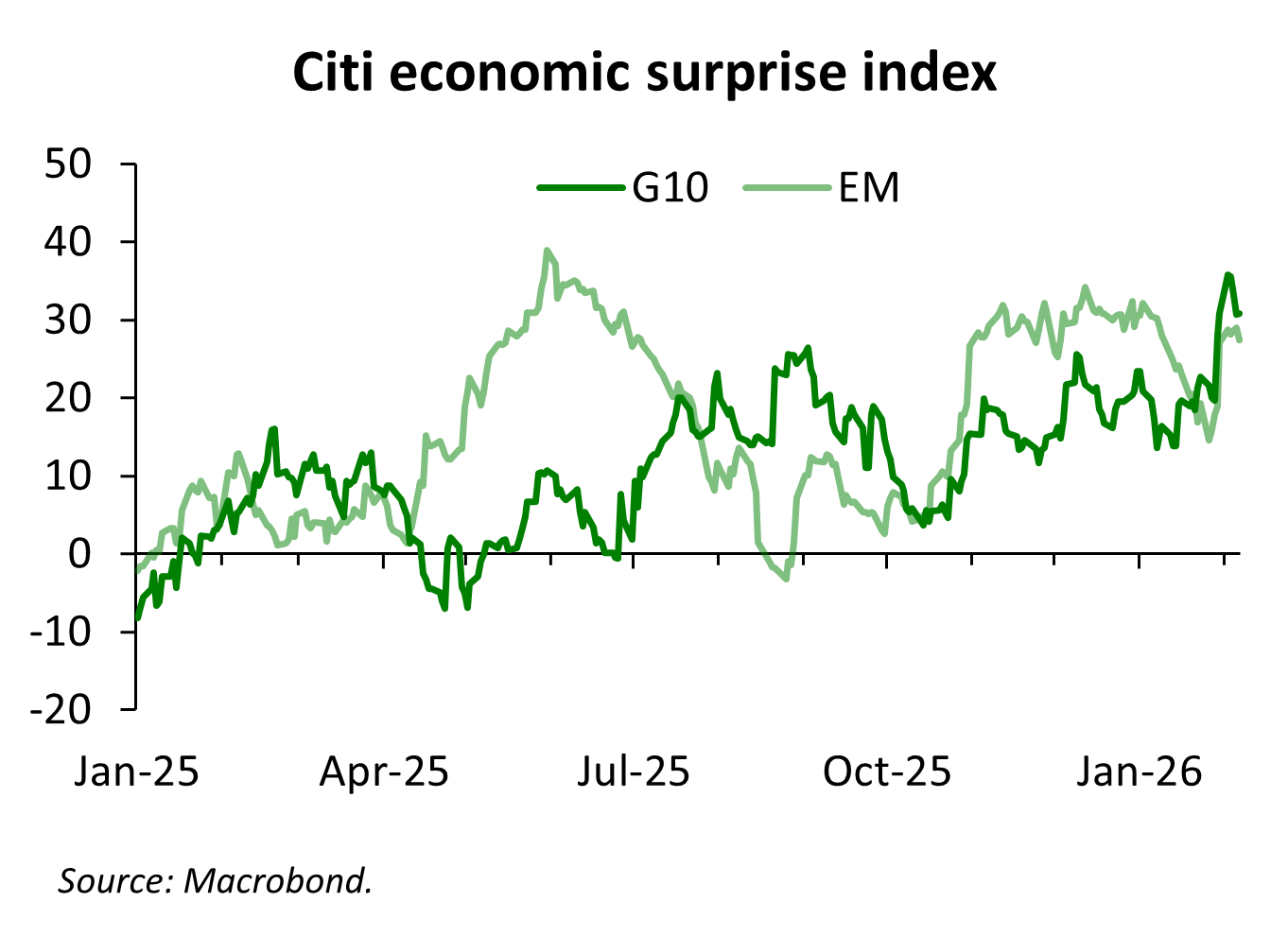

As expected, the Reserve Bank of Australia raised its cash rate target last week — after three rate cuts last year — and the Reserve Bank of India kept its policy rates unchanged. The RBA decision was a response, at least in part, to the rise inflation since Q2 last year. As January inflation data become available, we can see that in most economies in Asia Pacific — Thailand and New Zealand are notable exceptions — inflation appears to have stopped falling a few months ago and is now creeping higher. It’s too early to be talking of rate hikes, except in Australia, but with economic data in most large economies surprising to the upside — China is a very notable exception — the risks to inflation would seem to be tilting increasingly to the upside.

I’ll go through the Asia Pacific inflation trends at some length later, but first an update on tariffs.

India - US trade ‘deal’ hot on the heals of its EU agreement

Indian trade negotiators have been busy. Two weeks ago, India and the EU finalized a free trade agreement after more than three years of negotiations. Recall that the EU also at the same time wrapped up negotiations on a free trade agreement with Mercosur. On February 1, President Trump announced he’d made a ‘deal’ with President Modi to lower tariffs on mutual trade.

The deal was formalized in a joint statement on February 6. The deal is described as a framework for an interim agreement towards a fuller bilateral trade agreement which is still under negotiation (talks began in February 2025). The reaffirmation of the commitment to conclude those broader talks is perhaps the most important part of the statement. But there are some early wins.

Firstly, the 25% tariff applied on imports from India since August 6, 2025 as a penalty for India’s continued imports of oil from Russia has been removed. This is in response to commitments made by the Indian government that it will halt imports of oil from Russia and import more oil from the US and possibly Venezuela; and a commitment to expand defense cooperation with the US over the next 10 years. If India reneges on these commitments, Trump may reinstate this penalty tariff.

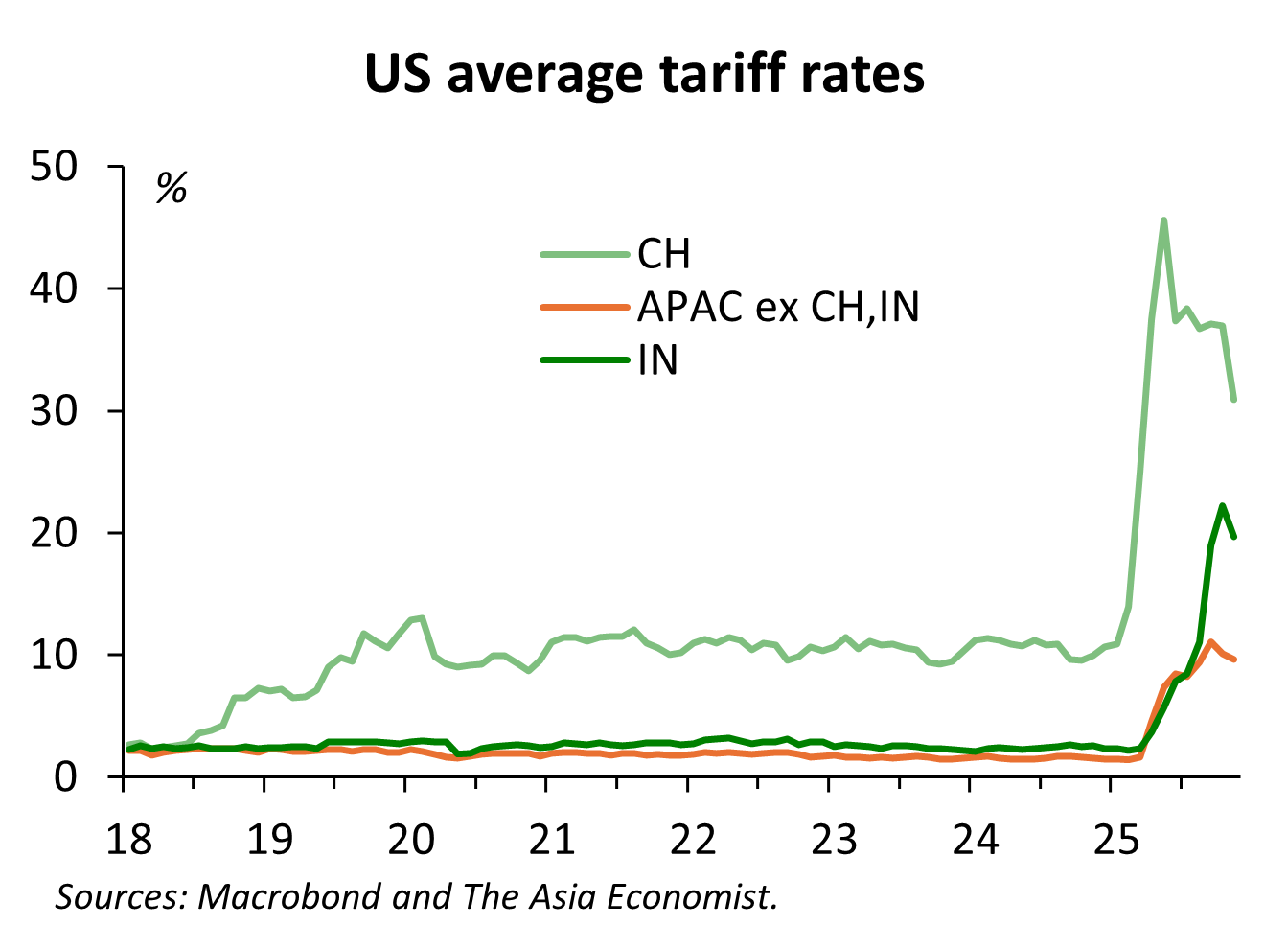

Second, the US will lower the 25% ‘reciprocal’ tariff applied to imports from India to 18%. This means the 50% tariff applied to Indian goods has been lowered to 18%. In fact, since nearly half of US imports from India weren’t tariffed, the average tariff rate actually applied to goods from India has been about 20% in recent months. The average tariff paid on imports from China has fallen from a peak of 46% in May to 30% in November. Even though since October the statutory tariff rate on imports from India has been higher than the rate applied to imports from China, the much lower ratio of dutiable imports (goods actually tariffed) in India means that overall the tariff rate on all imports from India has been much lower than the rate applied to all imports from China.

But Indian exporters have faced much higher tariffs than exporters from other economies, especially other Asia Pacific economies. The 18% tariff rate will now, assuming the previous exemptions continue to apply, likely bring the average tariff applied to imports from India down to the level of other Asia Pacific economies — i.e, around 9%.

The Section 232 tariffs on iron, steel, aluminium, copper and autos will continue to apply, but exemptions have been provided for some aircraft parts and automobile parts. The deal also includes provisions for lower tariffs on generic pharmaceuticals.

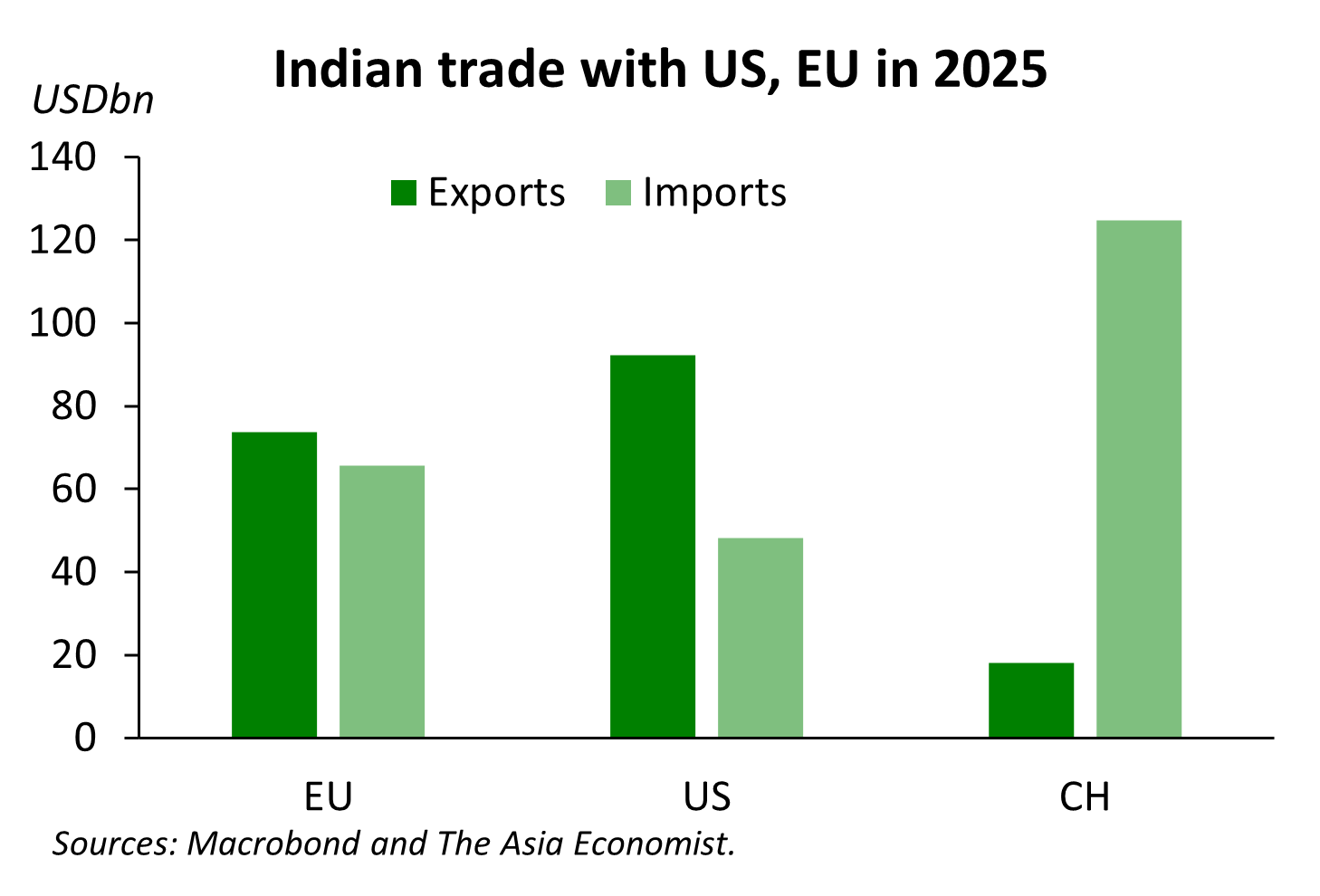

India has also agreed to purchase USD500 billion of US energy products, aircraft and aircraft parts, precious metals, technology products, and coking coal over the next five years. Some USD80bn of orders for Boeing aircraft are apparently imminent. Total Indian imports from the US last year were only USD48bn, so this USD500bn target over five years represents an enormous increase. India exported USD92bn to the US last year, so this USD500bn target would likely get trade close to balanced over the coming years if it is achieved.

Only a few days earlier, the Indian and EU governments had concluded talks on a free trade agreement that eliminates tariffs on almost all bilateral trade. This is a much fuller agreement than the US ‘deal’ — but the US and India are committed to reaching something similar in the near future.

Almost 97% of current EU exports to India will be tariff free by the time the agreement is fully in force. That will take some time. Tariff reduction is phased in over ten years but most will be removed in a 5-7 year timeframe. The Indian tariff on automobile imports from the EU is currently 110% but will be lowered to 10% — with a quota limit of 250,000 vehicles. The tariffs on EU wine and spirits will be cut from up to 150% to 20% - 40%.

The agreement also includes provisions for services sector liberalization. It also includes protections for intellectual property, including for geographical indications. This latter is important because the US has been requiring signatories to trade ‘deals’ in Asia Pacific to not protect geographical indications on food imports from the US.

Both sides kept some sensitive agricultural goods out of the deal — India will retain tariffs on imports of dairy products and cereals while the EU will retain tariffs on Indian sugar, meat, poultry and beef.

These two agreements with the US and EU apply to about 37% of Indian exports and 15% of its imports. The US, EU and China all account for just under 12% of total trade in India, but while India runs a trade surplus with the US and EU it runs a large deficit with China.

India has a mixed record and, frankly, a poor reputation when it comes to trade liberalization and there is considerable skepticism that it will be able to live up to these commitments. The FTA with the EU now must go through parliamentary approvals in both regions that could take most of this year (hopefully not more). The risk of backsliding as special interests push back on specifics is high but there’s no doubt that this is a monumental achievement. And for the EU to reach provisional agreement on FTAs with India and Mercosur sends a strong signal to Trump that it too is looking to diversify trade in response to US tariffs.

Trump applies tariffs on countries that trade with Iran, Cuba

As he had threatened, last week President Trump announced a 25% tariff on all imports from countries that trade with — import from — Iran and an unspecified tariff on countries that sell oil to Cuba.

The latter is part of his strategy of tightening the embargo on Cuba. After the extradition of Maduro and apparent takeover of the Venezuelan oil industry, Trump has ceased Venezuelan oil exports to Cuba. That leaves only Mexico, Russia and Algeria, reportedly, as suppliers of oil to Cuba. Mexico has been the largest supplier, even when Venezuela was still selling to Cuba and so this new tariff is mainly targeted at Mexico.

Mexico currently faces an average tariff of about 4.4% on its exports to the US (a tariff rate of about 26% is applied to only about 16% of its exports — the rest are exempt under USMCA. Canada faces an average tariff of about 3.7% because while it faces a higher de jure tariff rate slightly more of its exports are exempt. In late January, Trump threatened a 50% tariff on imports of Canadian aircraft but this has not yet been formalized as executive order.)

The Executive Order establishing this new tariff on oil suppliers to Cuba doesn’t specify how high the tariff will be and doesn’t even mandate that a tariff must be applied. After the Department of Commerce determines that a country is selling oil to Cuba, the Secretaries of Commerce, State and Treasury “shall determine whether and to what extent an additional ad valorem rate of duty should be imposed” and make that recommendation to the President who will then decide “whether and to what extent” to apply that penalty.

As I’ve noted since the beginning of January, the USMCA renewal negotiations are due to get underway in July. This Cuba oil tariff, like the threatened tariff on Canadian aircraft, must be viewed as part of that negotiation process. Trump is signaling a tough stance for the negotiations. Note that his reciprocal and sectoral tariffs likely already violate the USMCA because they weren’t preceded by a consultation with the other countries. But he’s adding more preconditions, it seems, to renewal of the USMCA. Note, for clarity, that if the talks fail it means the USMCA agreement will expire in 2036, not immediately.

The tariff on countries that trade with Iran is a little clearer — a tariff of 25% may be applied to any country importing any goods or services from Iran — although it provides the same wriggle room. The Secretary of Commerce may recommend a tariff be applied and the President may decide to apply it. Here again is tariff policy as signaling. The Executive Order was signed on Friday as Secretary Rubio was beginning talks with the Iranian government in Oman.

Iran is not an important trade counterparty for any Asia Pacific country. At least, not officially. Given the sanctions in place, companies have incentives to conceal trade with Iran. But the official data show that imports from Iran account for 0.1% or less of total imports in all regional economies. China, for example, reports total imports of USD3bn, which is 0.1% of its imports. India reports imports of USD408mn or 0.05% of total imports.

So if the US is serious about applying this tariff, it likely wouldn’t cause any real economic hardship for any country to completely cut off Iran. And even for China, the diplomatic cost is likely lower than the economic cost of a 25ppt increase in its tariff rate on sales to the US. There are other ways China can help Iran.

But again, how much of this is about trying to signal to Iran that there are still more ways the US can tighten sanctions versus part of an effort to impose pain on China’s exporters? I suspect the former is the dominant motive. In which case, this tariff may never actually be applied. Does Trump really want to risk blowing up his trade deal with China — and canceling his April state visit to China — over USD3bn of trade?

Lastly on the trade front, Trump announced a 80,000mT increase in the tariff-free quota of beef imports from Argentina on Friday. This is explicitly described as an effort to lower food costs in the US and so is a recognition by the White House that tariffs increase prices — even if the primary causes of rising beef prices are domestic supply shocks. Moreover, Argentine President Milei has made tariff reduction a key part of his economic program, opening up the economy as a way to encourage consumption and lower prices. Trump, of course, would disagree with this policy — he denies that tariffs increase prices even though they need to in order to have the effects he wants. But Friday’s announcement is an indication perhaps that the White House is slowly shifting its position.

Inflation is no longer falling in Asia Pacific

We got a host of inflation reports last week — from Indonesia, South Korea, the Philippines, Thailand, Taiwan and Vietnam — but the only notable report was Indonesian headline inflation, which jumped to 3.6% from 2.9%. But this was mostly because of a base effect from electricity subsidies last year that aren’t being repeated this year. Recall that Japanese headline inflation has fallen sharply recently because of the elimination of a gasoline tax.

Because of volatility in energy and food prices — due to taxes or subsidies or supply shocks — it’s preferable to monitor some measure of underlying inflation. Usually, that’s a measure of core inflation — CPI excluding volatile food and energy prices — but sometimes it’s a trimmed mean inflation rate, which excludes outliers even if they aren’t food or fuel prices.

Keep reading with a 7-day free trial

Subscribe to The Asia Economist to keep reading this post and get 7 days of free access to the full post archives.