Talking Points

The Philippines is the most exposed to economic shocks from the attack on Iran. China's Two Session start this week. Takaichi opposes BoJ rate hikes.

To the extent that there is a logic to Donald Trump’s foreign policy — and the suggestion that there is any logic to anything he does is often derided — it is that he is litigating decades-old grievances. It’s been said that his view of the world hasn’t changed since the early 1980s. Venezuela, Iran and Cuba have been persistent thorns and Trump is determined to resolve them once and for all with ‘regime change’ reinstating US dominance over their affairs. That’s the goal, at least. Even the idea of buying Greenland from Denmark has been around for a century or more. Why does he seem so positively inclined towards Russia? Because that’s an old Cold War rivalry that was long since resolved. He wants to put that and all these other conflicts behind the US so it can focus on the more important rival of the present and future: China. That’s the plan, at least.

So he must surely be hoping his assault on Iran can be finished as quickly as his decapitation of the Venezuelan regime was, or at least no longer than last year’s “12 day war”. I suppose we all hope so. I fear he’ll be disappointed though. Iran has broadened the scope of its response, threatening a regional conflagration and signaling, perhaps, that they see this as a battle for survival not just another in a sequence of attacks. Trump wants regime change in Iran, but the Iranian people can’t topple the regime unless it has been utterly defeated on the battlefield. That’ll take weeks of arial bombardment and, probably, boots on the ground.

A quieter battle is brewing, once again, between the government of Japan and its central bank. When Takaichi Sanae was elected LDP leader, many observers wondered whether she would give the Bank of Japan free rein to keep raising interest rates even while she pursued new fiscal stimulus. That question has, I think, been resolved. A leaked expression of “reservation” about the wisdom of hiking rates and the nomination of two clear doves to the BoJ Board proclaim loudly, I think, that the Prime Minister wants the BoJ to stop hiking rates. Without political cover, I think the BoJ will find it very difficult to raise rates again unless and until inflation is re-accelerating.

China’s Two Sessions get underway this week. Most important will be the release of the 15th Five Year Plan. There are unlikely to be many surprises in that document, but the formal adoption of the plan effectively gives government officials at every level their objectives and marching orders. I’ll be looking for evidence on how they’re planning to finance the investments in “new productive forces” beyond what has already been committed. We’ll also get the Government Work Report for 2026, which is likely to target a sub-5% growth rate.

The Bank of Thailand cut its policy rates last week for the sixth time in 17 months — by a total of 150bps, as I’d expected. But they signaled that they don’t intend to continue, calling on the government to provide stimulus by other means if necessary. The Bank of Korea, conversely, hasn’t cut its policy rates since May of last year. Inflation has hovered around the BoK’s target but property price inflation continues to accelerate even while mortgage lending slows. So too equity prices continue to rise rapidly, drawing households into more speculative investments. The balance of risks is tipping in the direction of rate hikes in South Korea to try to stabilize asset prices.

Note that South Korea reported its February trade data today. Exports to the US rose 29.9%yoy, essentially the same as in January. This is the fastest growth since the post-Covid reopening in 2021 and provides more evidence that the US ICT investment surge continues in Q1. This single fact underpins global markets and represents potentially the greatest risk to Asian economies if it should falter.

Iran

In the long history of US efforts to prevent Iran obtaining nuclear weapons, tariffs were probably the least likely tool to work. The 25% tariff applied on imports from countries that trade with Iran was announced on February 6 as US and Iranian negotiators prepared to meet. This is a war of Trump’s making: by all accounts (other than his), Iran was complying with the JCPOA but Trump withdrew US support in 2018, starting Iran back down on the path to nuclear weapons which has led us to this point after Trump’s usual dealmaking strategy — threats and bluster — didn’t impress the Iranians.

Meanwhile, more of his supporters are wondering if Trump isn’t, when all is said and done, a conventional Republican president: tax cuts for the rich, spending cuts for the poor, and war in the Middle East. This is a risky war for domestic political reasons, not just geopolitical ones. Trump is gambling on a quick, decisive and (for Americans) bloodless, victory to bolster his ratings. If he doesn’t get it, the Republicans will pay dearly come the mid-terms.

Look elsewhere for your OSINT. “The first casualty of war”, etc. Don’t get caught up in the excitement of the first hours. Iran has already broadened the conflict to include countries hosting US forces in the region. They have more to lose than Trump and will fight as long as they can. Trump is overtly aiming for regime change, and not the Venezuelan type where the leader goes but the same corrupt regime stays. Trump has promised the Iranian people they will be able to overthrow their government when he’s done. While the US and Israel can, over time, probably destroy most Iranian military capabilities with air strikes, that doesn’t remove the government or the IRGC. That is likely to require ‘boots on the ground’ something Trump and his supporters are loathe to do.

What does this mean for Asia Pacific? The most immediate risk is from higher oil prices. Crude oil has already risen more than 20% since the beginning of the year and will likely jump higher on Monday. China will have to replace some 1.4mn - 1.8mn bb/d of supply (this had risen to about 2.2mn bbl/d recently) while the Strait of Hormuz, even if not completely closed, will likely see drastically lower traffic out of caution. OPEC have agreed to increase production from April onwards by 206,000 bbl/d not enough to replace Iranian exports.

So oil and petroleum product prices will rise. Credible guesses say we can expect USD100/bbl soon. Whereas energy has been a deflationary factor for the past 18 months as oil prices fell, it will now be an inflationary factor. Crude oil at USD100/bbl in March would by nearly 40% higher than a year ago.

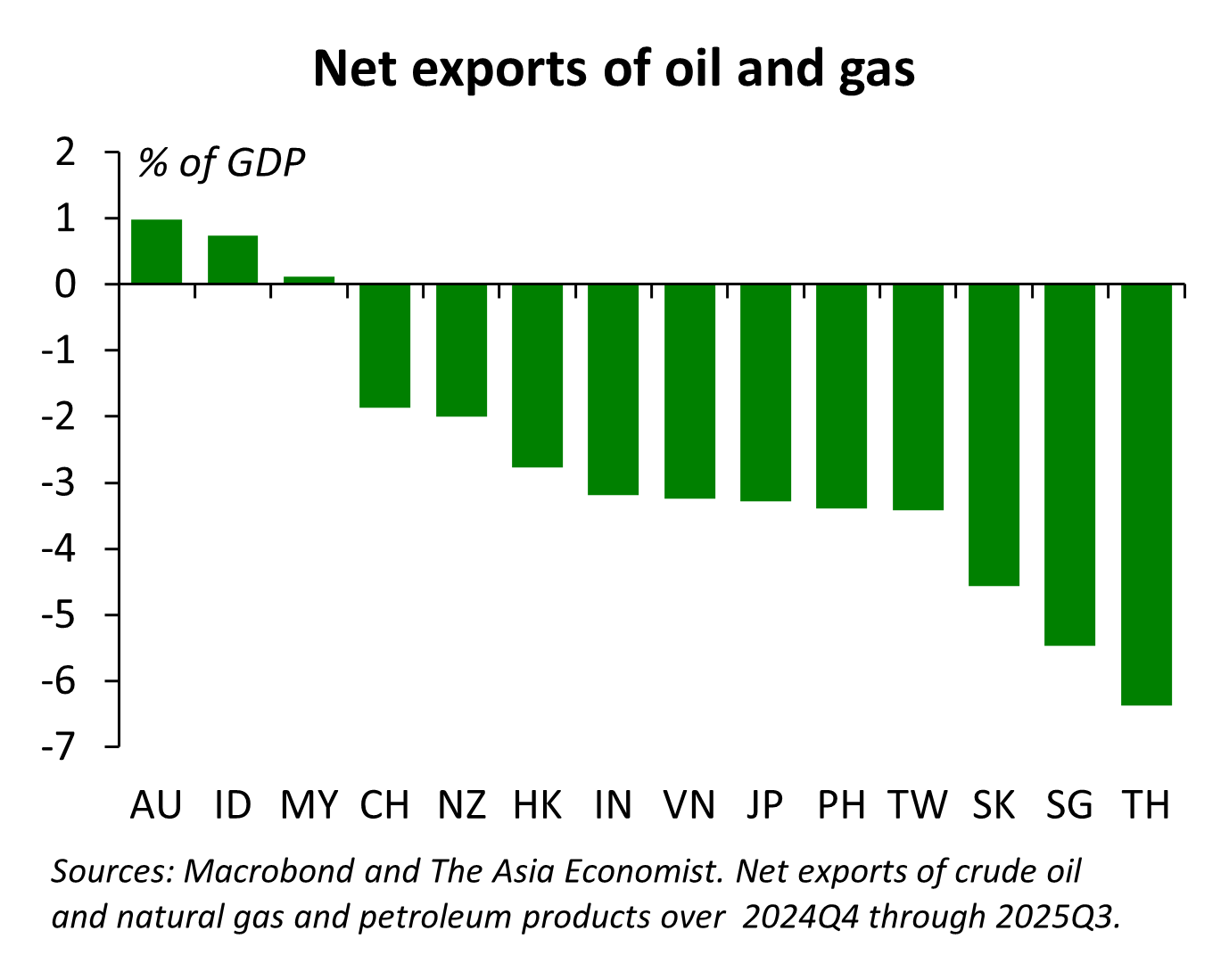

The increase in oil and gas prices will benefit Australia, Indonesia and Malaysia, which are modest net exporters, but tax the rest of the region, especially Thailand. (To some extent this chart exaggerates the exposure of some countries by not including net exports of petrochemicals and other products for which gas is a feedstock but aren’t classified as oil and gas products.)

But even where countries are net exporters, and generally where they are importers, a rise in the world prices of oil and gas may be passed on to consumers. The greater the reliance on imports and the smaller the tax imposed on petroleum, the greater is the potential passthrough unless governments choose not to allow retail prices to rise, in which case there will be a commensurate rise in the fiscal deficit.

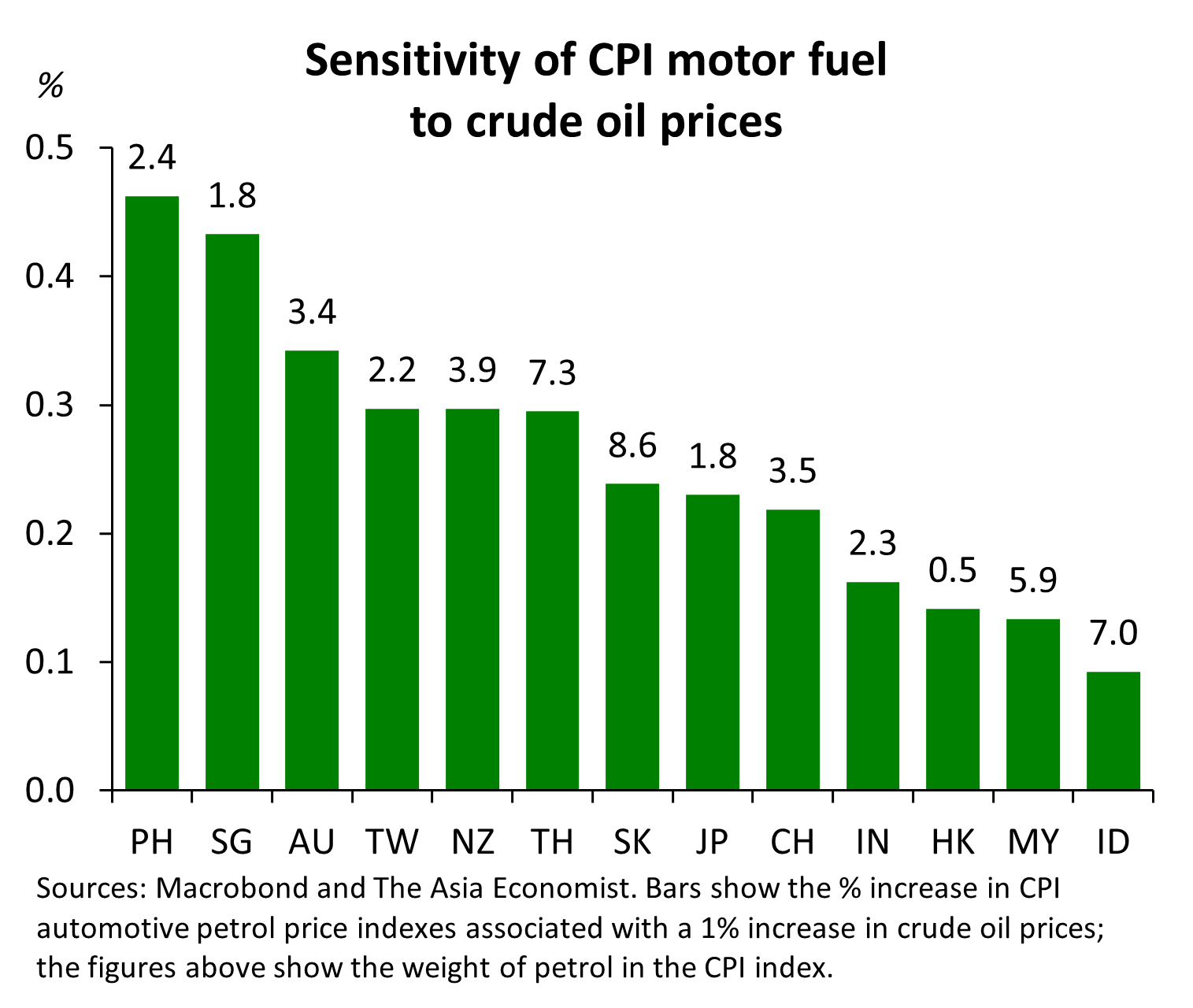

The estimated passthrough to consumers is greatest in the Philippines, Singapore, and Australia. By contrast in Indonesia, Malaysia and India, consumer prices don’t vary much in response to oil price shocks. The low sensitivity of consumer prices in Hong Kong reflects the high tax burden on petrol, which dampens the effect of fluctuations in crude oil.

So a spike in crude oil (and gas) prices in response to the war in the Middle East will increase the oil and gas import bill — manageable in a region of mostly trade surplus economies — but tax consumers to the extent the shock is passed on to them. India and the Philippines, with persistent and large trade deficits, face probably the biggest risk to currency stability. The Philippines is also probably the most exposed to a domestic inflation shock.

The longer the conflict goes on, the greater these costs will be.

China’s Two Sessions start this week

Iran will likely dominate investor attention outside Asia this week, but China’s annual NPC/CPPCC meetings will begin on Wednesday (CPPCC) and Thursday (NPC) and run probably for a week. Hopefully, events in the Middle East will allow us to focus some attention on these meetings because they are particularly important this year.

Most important, the 15th Five Year Plan will be presented. We know much already about the likely contents, including from the Recommendations of the Central Committee released last October and it’s unlikely the final Plan will deviate much from that document. But the Two Sessions will give every official in China their new objectives and will sanction financing for new projects and priorities.

The 15th FYP starts from the perspective that the previous drivers of growth in China — property and export-oriented industries — are weak and rather than try to revive them the focus should be on “new productive forces”. That is, new technologies and new industries to drive higher productivity growth so that real GDP growth per capita can be maintained. This is the goal all countries have, but it is the unrelenting focus of this government.

As in the US, an important part of the promotion of new technologies is to achieve technological self-sufficiency. While the FYP will talk about partnering with other countries and promoting two-way FDI, the reality is that the government expects that China must win the battle for technological supremacy by itself. So I’ll be looking at how they intend to finance all this new investment.

At the same time and with a shorter horizon, the Government Work Report will set out objectives for 2026. This report may for the first time set a goal for GDP growth below 5%. Even if the new target is 4.5% - 5.0% or “close to 5%”, the message is that fiscal or monetary stimulus will not be needed in the near-term, only if the economy slows sharply. As I’ve been saying for a while, with core inflation rising, the PBoC will be much less inclined to ease monetary policy significantly. But on the fiscal front, I think the government will be counting on financing of new FYP priorities providing a new growth impulse rather than tax cuts or more handouts to consumers.

I expect consumption growth to be a priority of the FYP; it won’t just be about new technologies and industries. I think we may see new policies to raise the social safety net — childcare and elder-care facilities, pension reform, etc — to try to reduce the precautionary savings motive.

But broadly, the message will be that the government will continue to look to newly emerging industries and technologies to boost growth rather than trying to prop up the property market or subsidise consumption or cutting interest rates to encourage new borrowing by old industries.

Takaichi takes on the BoJ

Keep reading with a 7-day free trial

Subscribe to The Asia Economist to keep reading this post and get 7 days of free access to the full post archives.