Where to now?

It is a strange sort of ceasefire that allows the two sides to keep shooting at each other, but it is the ceasefire we have. The Islamabad Memorandum rewards Iran for reopening the Strait of Hormuz by removing all US and UN sanctions, allowing for the resumption of all Iranian trade, including oil exports, unfreezing Iranian assets in the US and dangling the prospect of a USD300bn reconstruction fund. The MOU doesn’t rule out the imposition of some kind of toll levied by Iran on shipping after 60 days. Iran has, again, committed to not acquiring or developing nuclear weapons but the MOU offers the possibility that its enriched uranium stockpile will be diluted on-site rather than removed. President Trump is so proud of this MOU that you won’t find it on any US government website. The only copy of the signed document I can find is on the Iranian government’s X account.

The MOU makes so many concessions to Iran that I think it shows how desperate Trump is to end the war. It has elicited harsh rebukes of the administration even from Republicans, but I think it is safe to conclude that the war is over.

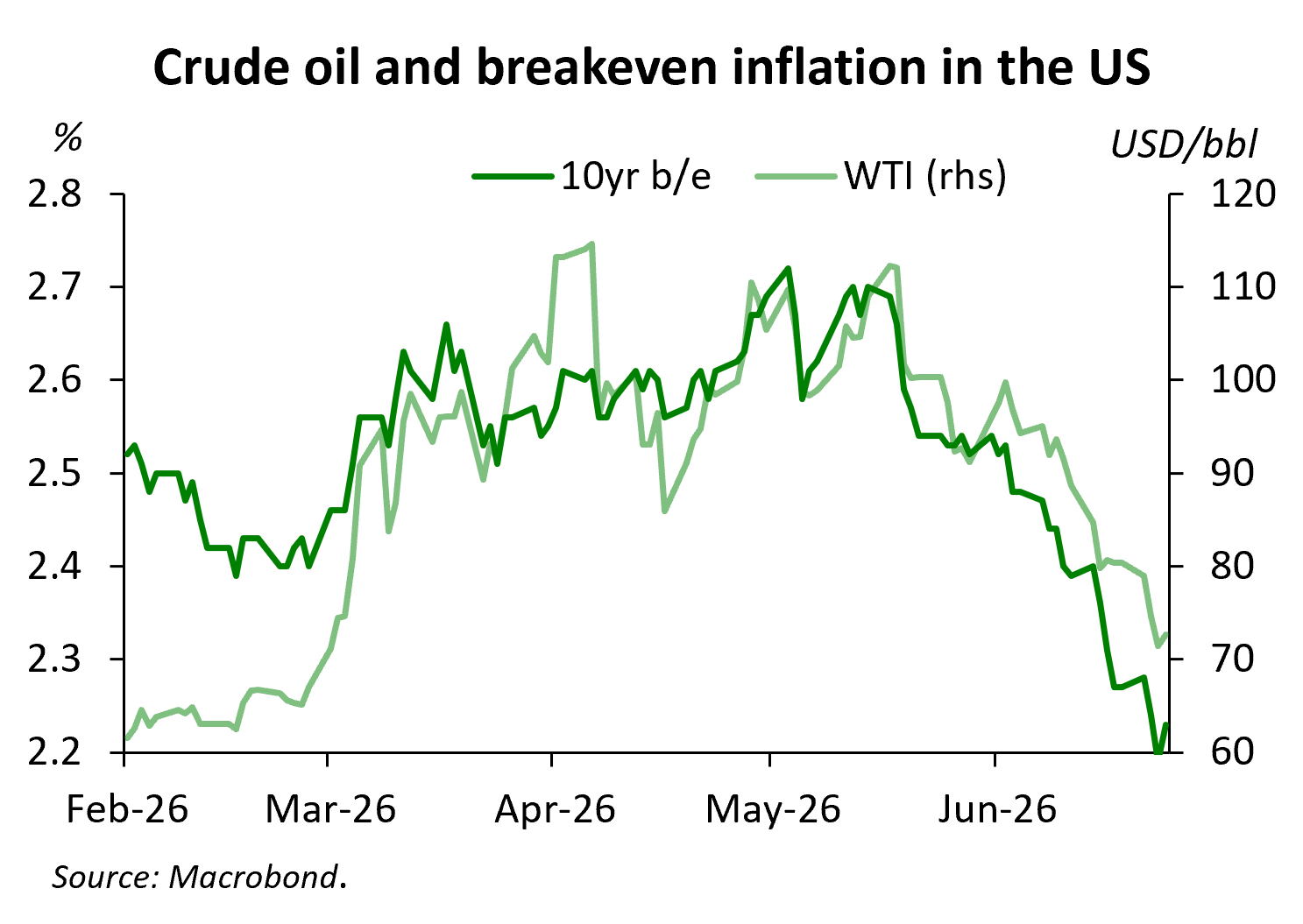

Inflation expectations are plummeting as the oil shock reverses

So crude oil prices have retraced almost all of their wartime surge and breakeven inflation rates are lower than they were when the war began. In the market’s view, all of the inflation risk from the war has gone. More than that: investors have concluded that the US economy is less inflationary today than it was in February. The same is true in Germany, by the way.

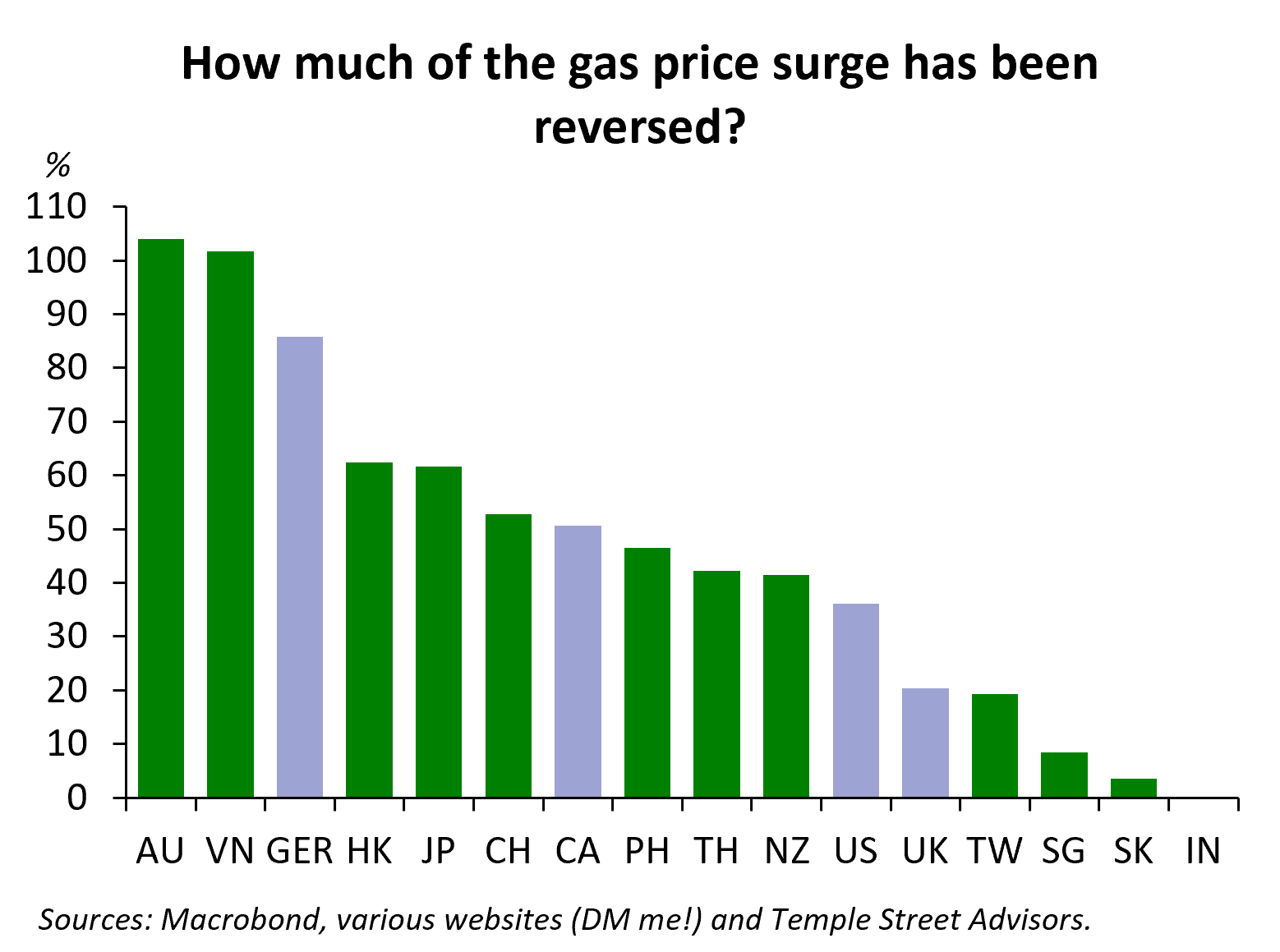

It’ll take a while longer for retail fuel prices to normalize than it has for crude. In the US, gas prices started falling in early June but have only reversed just over one-third of the peak rise in prices. Prices have only just begun to decline in the UK but are well on the way to normalizing in Germany. Most other European economies are somewhere between these two markets.

Gasoline prices in Australia and Vietnam, though, are already lower than they were on the eve of the war. In Hong Kong, Japan and China prices have retraced more than half of the post-war surge. But in Singapore, South Korea and India, prices have barely begun to decline. Admittedly, in India prices only rose about 8%. But they rose about 20% in Singapore and South Korea and are still almost 19% higher than their pre-war levels. In Indonesia and Malaysia, most consumers have been spared from any price increase. So subsidy costs may be falling but there’s much less of an energy inflation surge to reverse.

But as crude oil declines are passed on to consumers headline inflation is likely to decline and consumers’ fears about inflation may ease. That is, it’s believed, an important part of President Trump’s motivation for ending the war. He needs to defuse inflation as a political liability before the mid-terms.

A hawkish Fed? Really?

As he has not been shy to tell us, Trump also wants — expects, even — the Fed to cut rates as inflation eases. We clearly got the opposite signal from the Fed on June 17 as I discussed last week. But I am of the view that that was Chair Warsh trying to convice us he’s a hawk when in fact he’s a dove. As I noted last week, the only change to the description of the economy’s current state that Warsh made in the now much shorter statement was to insert a reminder that “productivity growth and capital investment are strong”. In campaigning for the job, Warsh had argued that technological advances like AI are disinflationary and that its adoption could lead to lower (nominal) interest rates.

And Warsh made sure to tell us that the only option on the table on June 17 was a pause. This supposedly hawkish Fed Chair, faced with a Committee the majority of whose members want to raise rates, didn’t even give them that option.

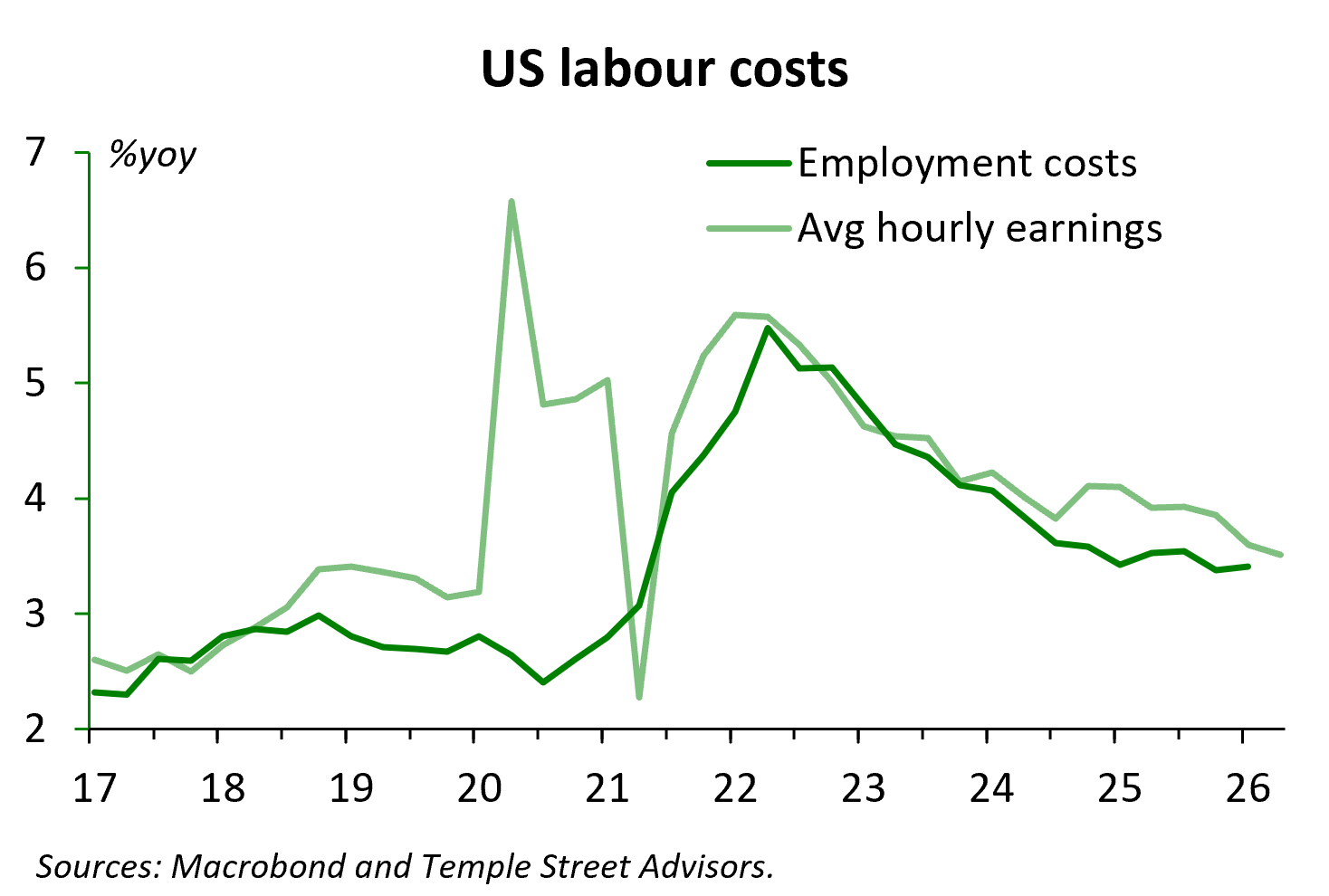

I think Warsh is hoping to be able to argue at the July 28-29 FOMC meeting that the wartime inflation risk is gone and that with AI adoption likely to push inflation down, there is no need for the Fed to hike rates. He’ll probably point to breakeven inflation rates below their pre-war levels as supporting evidence. It would probably be too much to tilt back to an easing bias — the labour market’s too strong for that — but slowing wage inflation also supports what I think is a dovish Chair view.

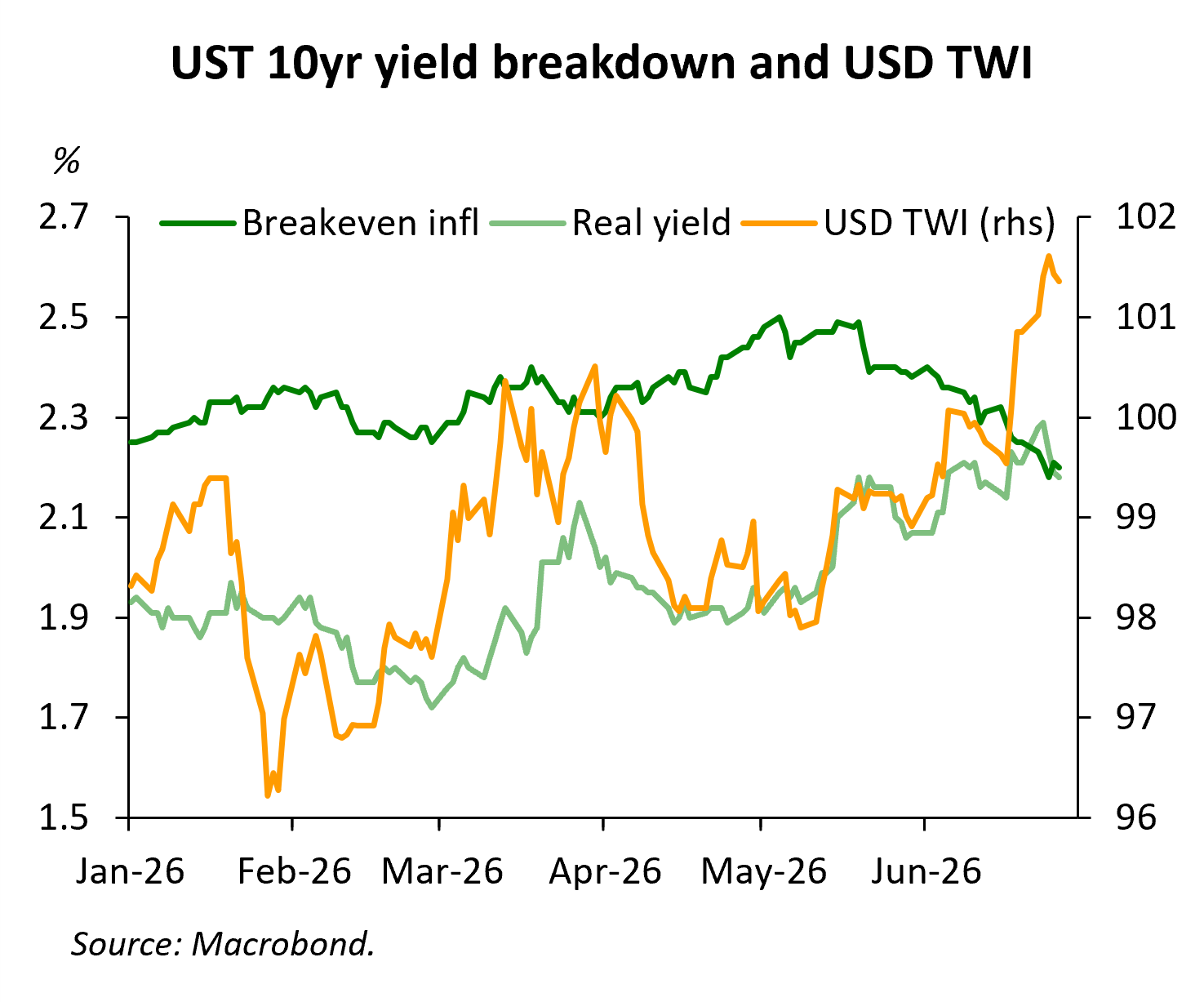

Taking out the rate hike wouldn’t necessarily lead to lower real rates in the US. But the strength of the dollar in recent weeks is strikingly different from the weakening that we saw when the ceasefire was first announced in April. Then, real yields were falling as inflation expectations were rising and the dollar fell sharply. Now, with inflation expectations falling since mid-May, the hawkish Fed has pushed real yields even higher and the dollar has risen to its strongest level against other advanced economies since May 2025. And most APAC currencies also have depreciated against the dollar.

We should see the same dynamics at work in APAC: lower oil prices feeding into lower fuel prices for consumers and likely lower headline inflation. That will take some of the pressure off central banks to hike rates. And if the Fed does in fact sound less hawkish in a months’ time, that will go a long way towards supporting APAC bonds and currencies.

Growth survived the oil shock

If inflation is about to start declining, what can we say about the rate of growth of the US and APAC economies? During what has been decribed as the worst ever supply shock to energy, economic growth has held up surprisingly well in most places.

This is in large part because of the release of strategic petroleum reserves, which served to put a cap on oil prices. In the US alone, some 84mn bbls was released from the SPR, taking the reserve to its lowest level in 43 years. IEA members pledged in early March to release 400mn bbls from reserves. China started the war with an estimated six months’ worth of oil consumption in reserve. Its oil import volumes fell about 16%yoy in March - May, suggesting the strategic reserve may have been drained by about 8%. But production in some oil-intensive industries — e.g., plastics, petrochemicals — was sharply lower after February, so it’s possible that not all of the decline in oil imports was offset by releasing reserves.

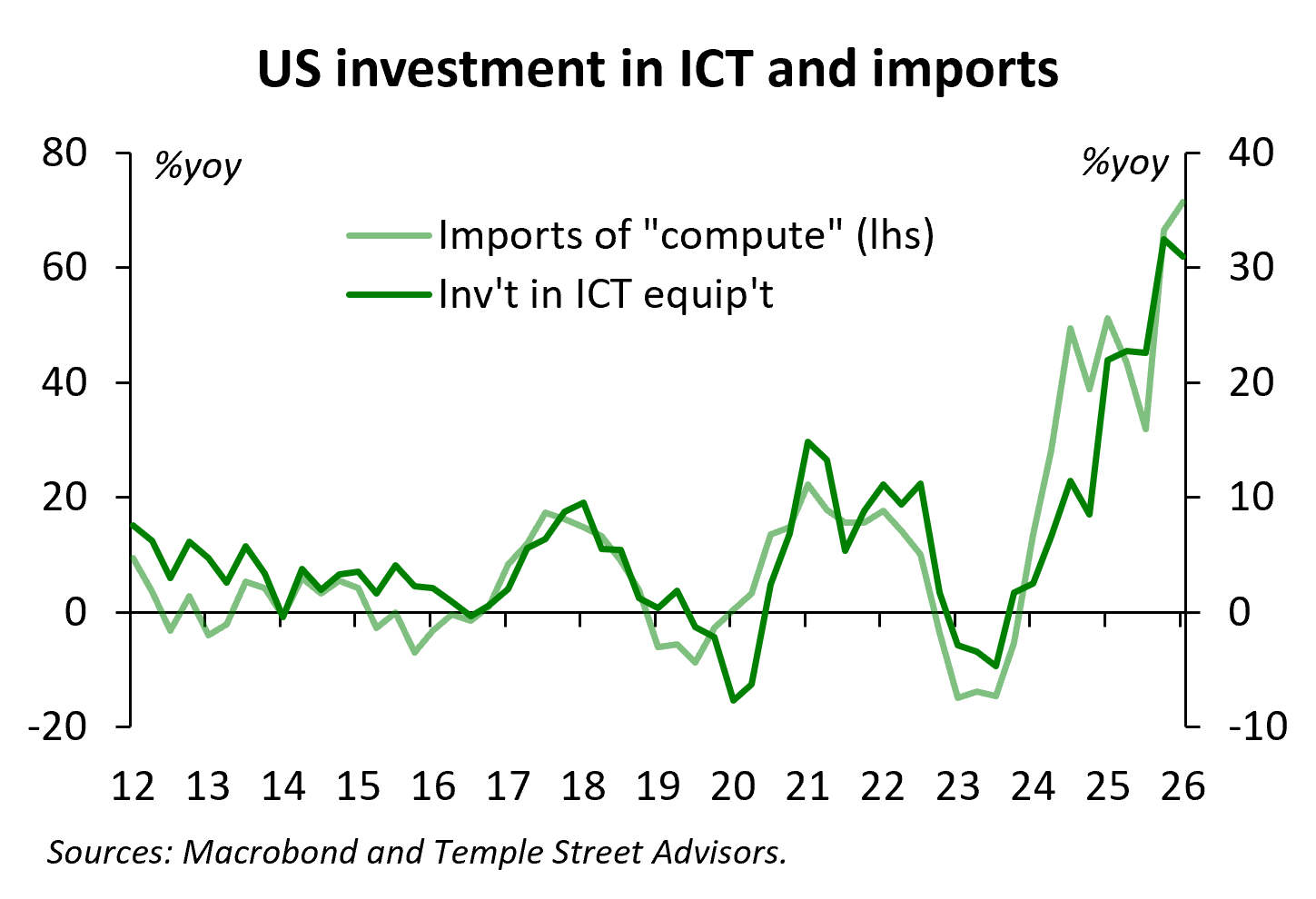

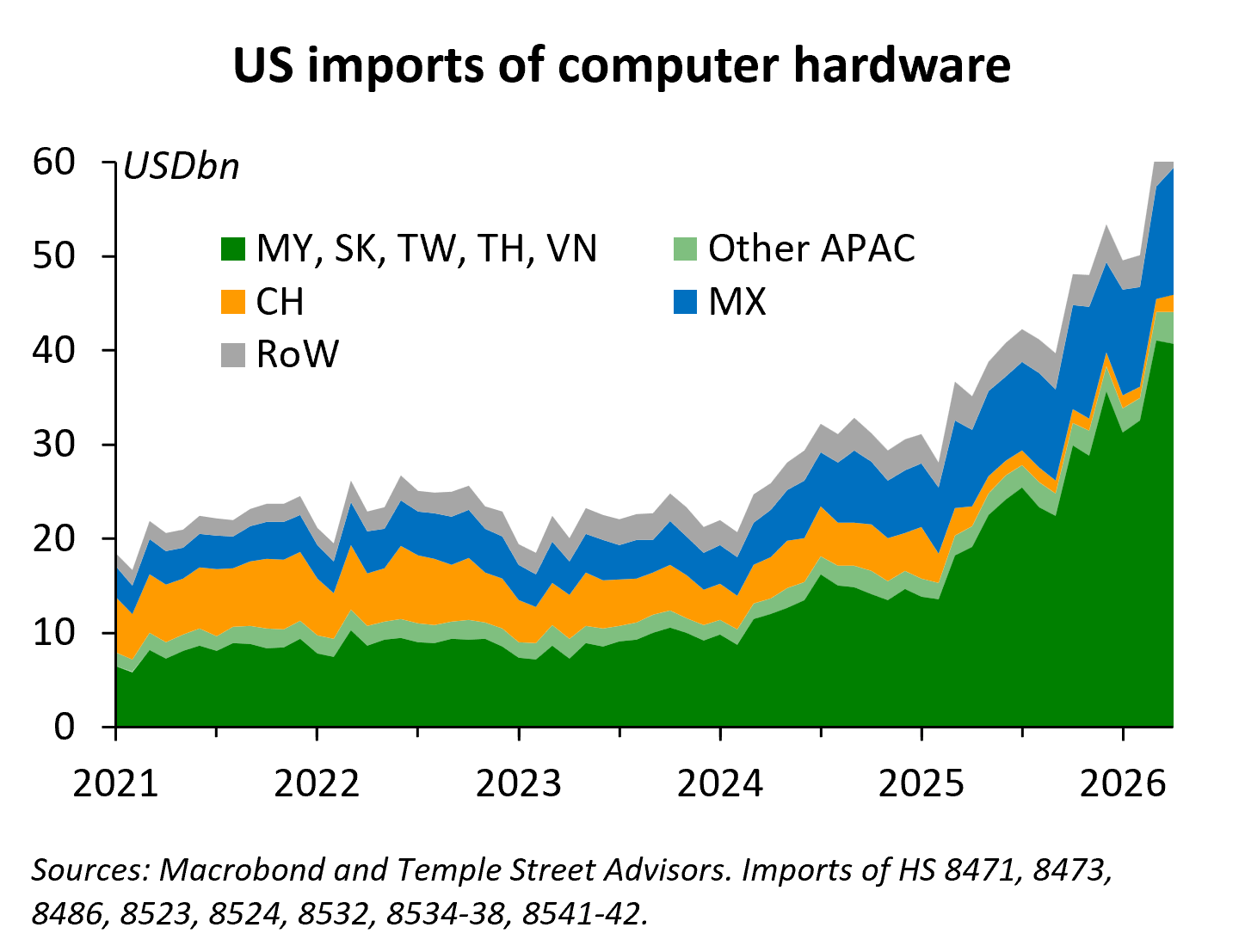

But the resilience of the US and APAC economies was also in large part due to the fact that growth has increasingly come from less oil-intensive industries. US investments in ICT hardware and software/R&D accounted for two-thirds of GDP growth in Q1 and a similar share of growth in the previous three quarters. And that doesn’t include investment in power generation to support data centers. That spending on ICT hardware is very import-dependent, so imports of computer-related equipment have grown remarkably quickly over the past year as this AI-related investment boom has expanded.

And most of those imports come from Mexico and five APAC economies: Taiwan, Vietnam, Thailand, South Korea and Malaysia. These six economies account for about 80% of US imports of computer hardware and components. China, as a direct source of US imports, was largely squeezed out by last year’s tariffs.

So strong US demand for computer hardware — everything from semiconductors to displays and keyboards — has supported these economies. I would add the Philippines to the group because even though it is a small supplier from the US’ perspective, exports of computer components account for well over half of Philippine exports to the US, which is the Philippines’ largest export market.

From the US side, data show imports of computer equipment rising 81%yoy in April, which is a record high. But imports have been growing at an average rate of 68% over the past seven months. Taiwan was the initial beneficiary — its exports of semiconductors and other computer hardware rose 215%yoy in Q4 last year up from 86% in Q3. Growth has since eased to 71% in April/May. But exports from Malaysia and South Korea have accelerated sharply during this time. Malaysian exports of electronics products to the US more than doubled in May and South Korea has seen growth of more than 150% in April and May.

So from the perspective of Asian exporters, the AI investment boom not only continues but may still be accelerating. And that rising export growth is fueling stronger consumption. In South Korea and Taiwan, even as retail fuel prices unwind their post-war increase, I think central banks should still be raising interest rates.

China trade returns

In fact, it’s probably easier to identify the economies that don’t appear to be benefitting directly from the US investment surge: Australia, India, Indonesia and New Zealand. But even if their exports to the US aren’t growing especially quickly, they are seeing faster growth in sales to China recently. Why?